I keep noticing something strange about Nike...

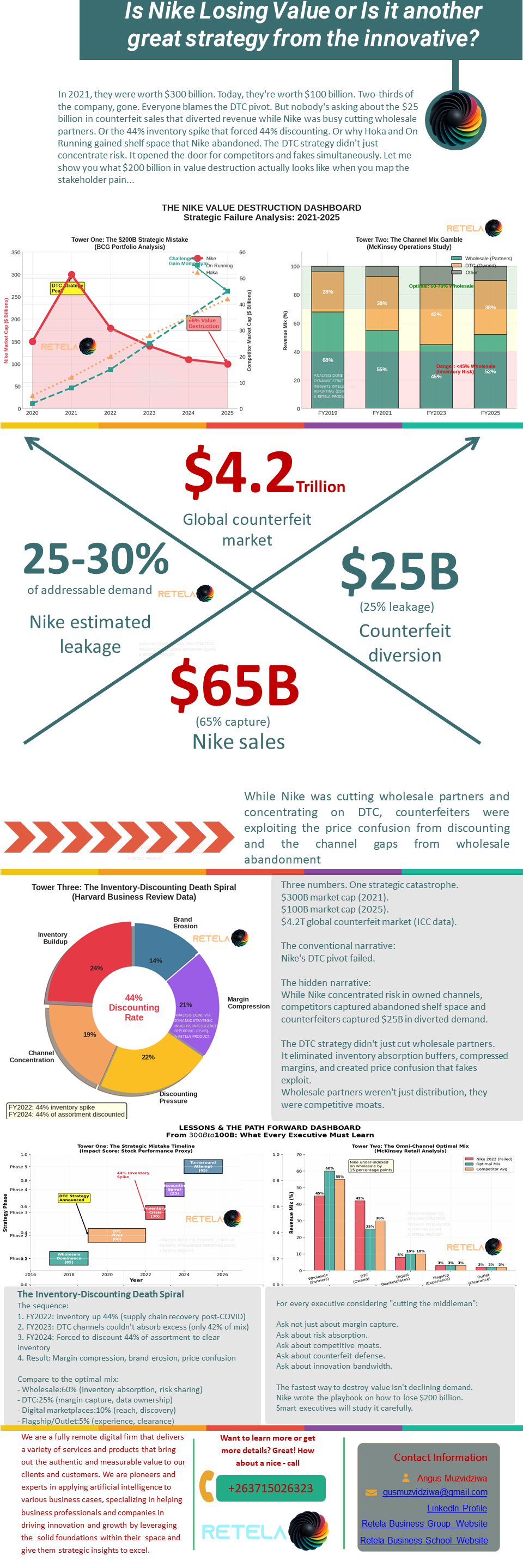

In 2021, they were worth $300B.

Today: $100B. Two-thirds gone.

Everyone blames the DTC pivot.

But nobody’s asking about the $25B in counterfeit sales that diverted revenue while Nike cut wholesale partners.

Or the 44% inventory spike forcing 44% discounting.

Or why Hoka and On Running gained shelf space Nike abandoned.

DTC didn’t just concentrate risk. It opened a two‑front war: competitors and fakes simultaneously.

The Value Destruction

- 2021: $300B market cap

- 2025: $100B

- Meanwhile: On Running $2B → $45B; Hoka $5B → $42B.

The Channel Gamble

2019: 68% wholesale, 28% DTC

2023: 45% wholesale, 42% DTC

Second-order effects:

- Inventory concentration (DTC held 42% of load)

- No wholesale buffers → 44% of assortment discounted

- Competitors captured abandoned shelf space (Nike lost 7pp premium shelf)

The Counterfeit Leakage

Global counterfeit market: $4.2T. Nike leakage: ~$20‑25B annually.

DTC created price confusion and channel gaps that fakes exploit.

Stakeholder Pain

- Wholesale partners: lost allocation, trust frayed

- Employees: 775+ layoffs, 401(k)s crushed

- Investors: $200B market cap wiped

- Consumers: price confusion, authenticity risk

Recovery Scenarios (Recommended)

Hybrid omni‑channel: 60% wholesale, 25% DTC, 15% other.

NPV upside: +$25B vs. status quo.

Executive Lessons

1. Channel concentration risk – never >40% in one channel.

2. Inventory absorption – wholesale partners buffer demand shocks.

3. Wholesale partnerships = competitive moats. Shelf space is expensive to reclaim.

4. Innovation discipline – channel complexity diverted R&D; Nike’s innovation score dropped 25 points.

5. Counterfeit defense – distribution breadth deters fakes.

The $200B Lesson

DTC isn’t inherently risky. Concentration is.

Distribution is strategy. Channel mix is risk management.

Before cutting middlemen, ask:

- Risk absorption?

- Competitive moats?

- Counterfeit defense?

- Innovation bandwidth?

What’s your channel concentration risk?

Comments ()