VAR Models in Stata - DO File + Slides + Dataset

On Sale

$4.99

$4.99

This package contains all the material covered in my two YouTube Video "VAR model in STATA".

The package includes:

1-DO File - Complete and detailed, step by step

2-Video Slides

3-Data Set

I hope you enjoy it!

JD Economics.

The package includes:

1-DO File - Complete and detailed, step by step

2-Video Slides

3-Data Set

I hope you enjoy it!

JD Economics.

Estimating VAR Models in Stata: A Step-by-Step Guide

Vector autoregressive (VAR) models are a powerful tool for analyzing multivariate time series data. In this guide, I'll provide you with everything you need to estimate VAR models in simple steps. Get the complete DO file, data set and slides of my video!

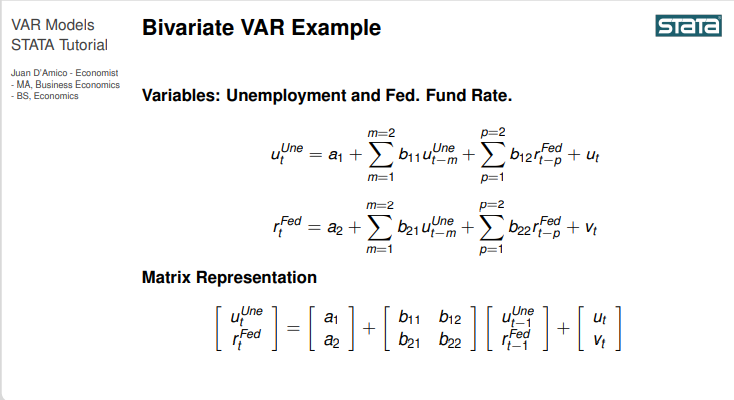

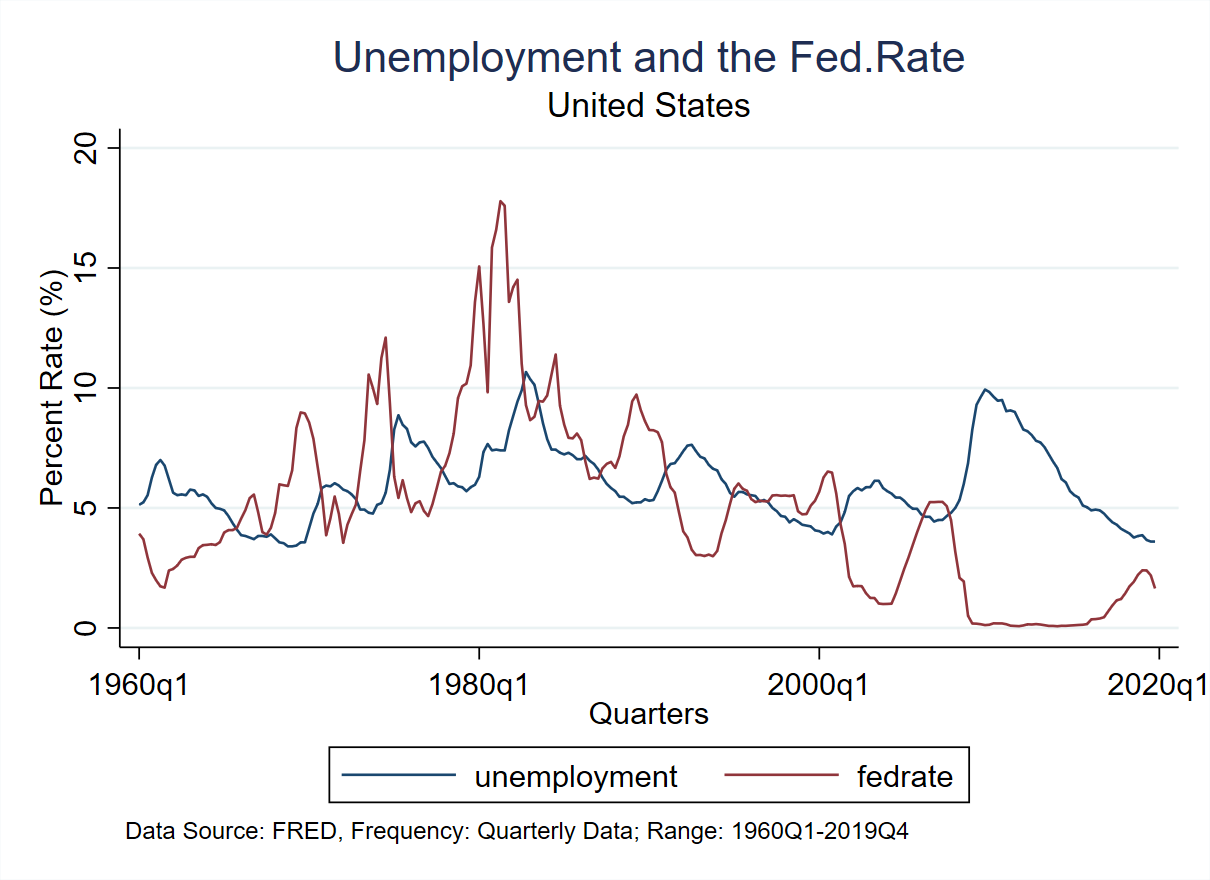

Real Example

We estimate a VAR model to understand how unexpected changes in unemployment affect the Fed. Rate.

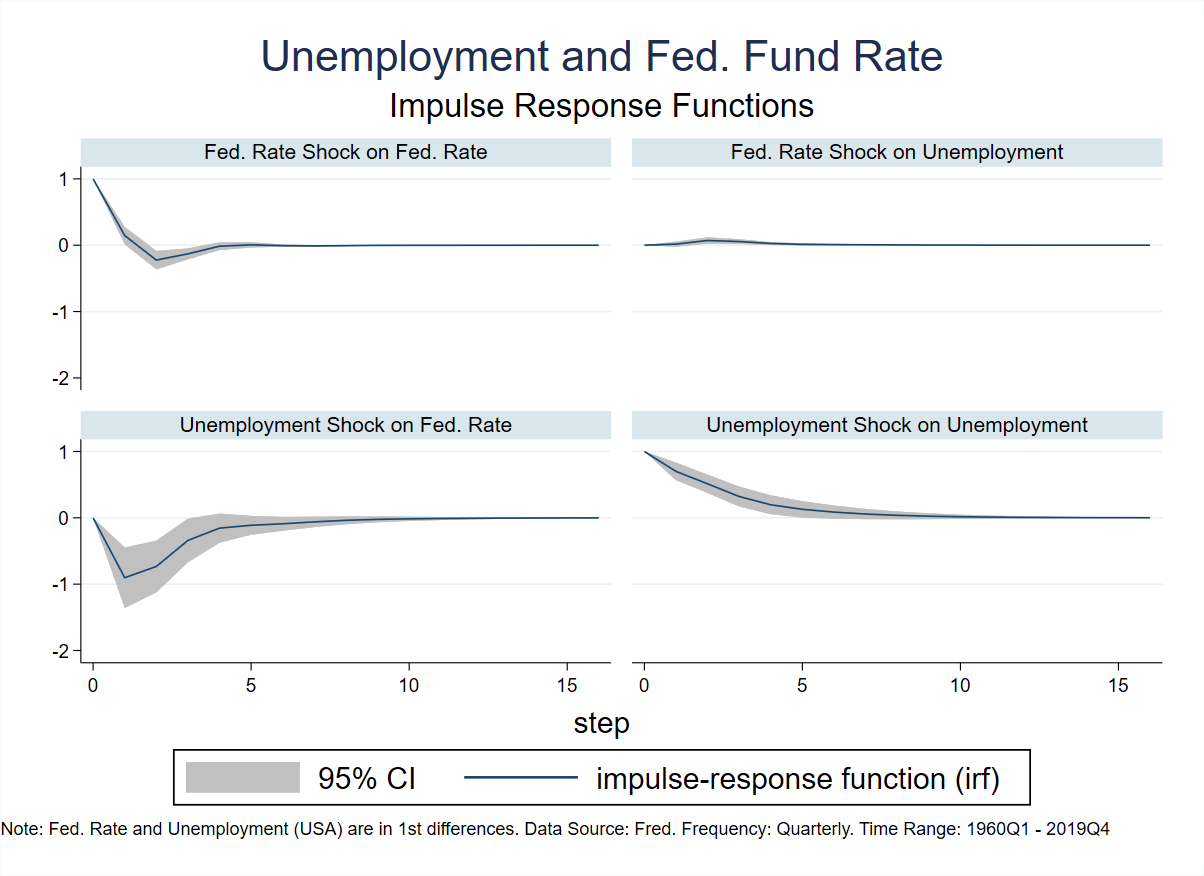

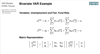

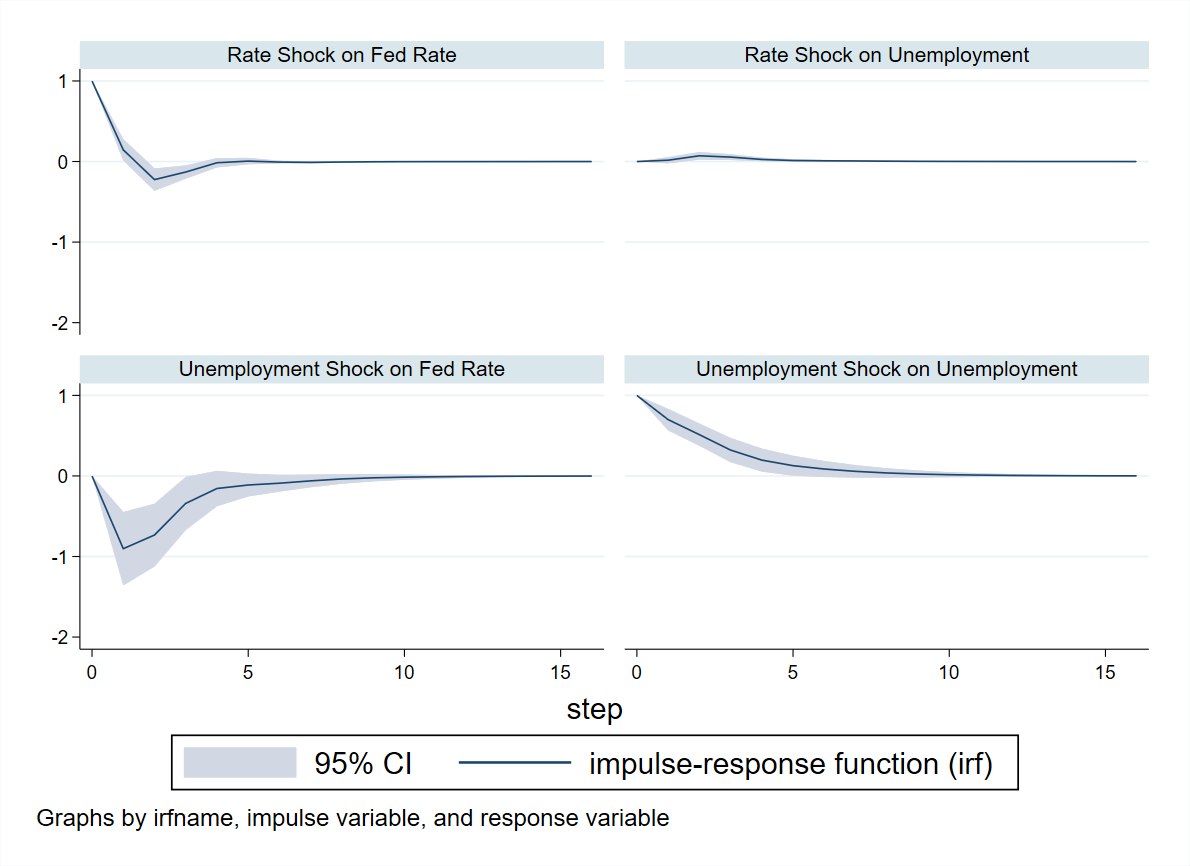

Impulse Responses

Examine the responses of the endogenous variables to unexpected shocks. It becomes evident that when there is a positive shock in unemployment, the Federal Reserve responds by decreasing the interest rate. We can interpret this as an expansionary reaction to a contractionary unemployment shock.

Customer Reviews

You may want to consider buying the bundle..

Get the files to estimate ARIMA models, Cointegration and Error Correction Model (Engel and Granger method) and VAR Models.

Stata Bundle - ALL FILES IN 1 PACKAGE

On Sale

$21.99

$21.99

Save by getting this bundle!

You will get the slides, DO File, and datasets for all my available tutorials:

1-ARIMA Models

2-Produce forecasts with AR Models

3-Cointegration and Error Correction Model (Engel and Granger method)

4-VAR models

5-VAR models Forecast with confidence bands

Plus, the free content:

i. Generate Tme Series Variables

ii. Produce professional Graphs in Stata

You will get the slides, DO File, and datasets for all my available tutorials:

1-ARIMA Models

2-Produce forecasts with AR Models

3-Cointegration and Error Correction Model (Engel and Granger method)

4-VAR models

5-VAR models Forecast with confidence bands

Plus, the free content:

i. Generate Tme Series Variables

ii. Produce professional Graphs in Stata