Most buyers start with one question:

“How much can I afford?”

And the answer they get is usually based on what the bank is willing to lend — not what is actually comfortable to repay.

In today’s market, that difference matters.

With rising living costs and the possibility of further interest rate increases, buying at your maximum approval level can quickly become financially stressful.

💰 What Most Buyers Get Wrong

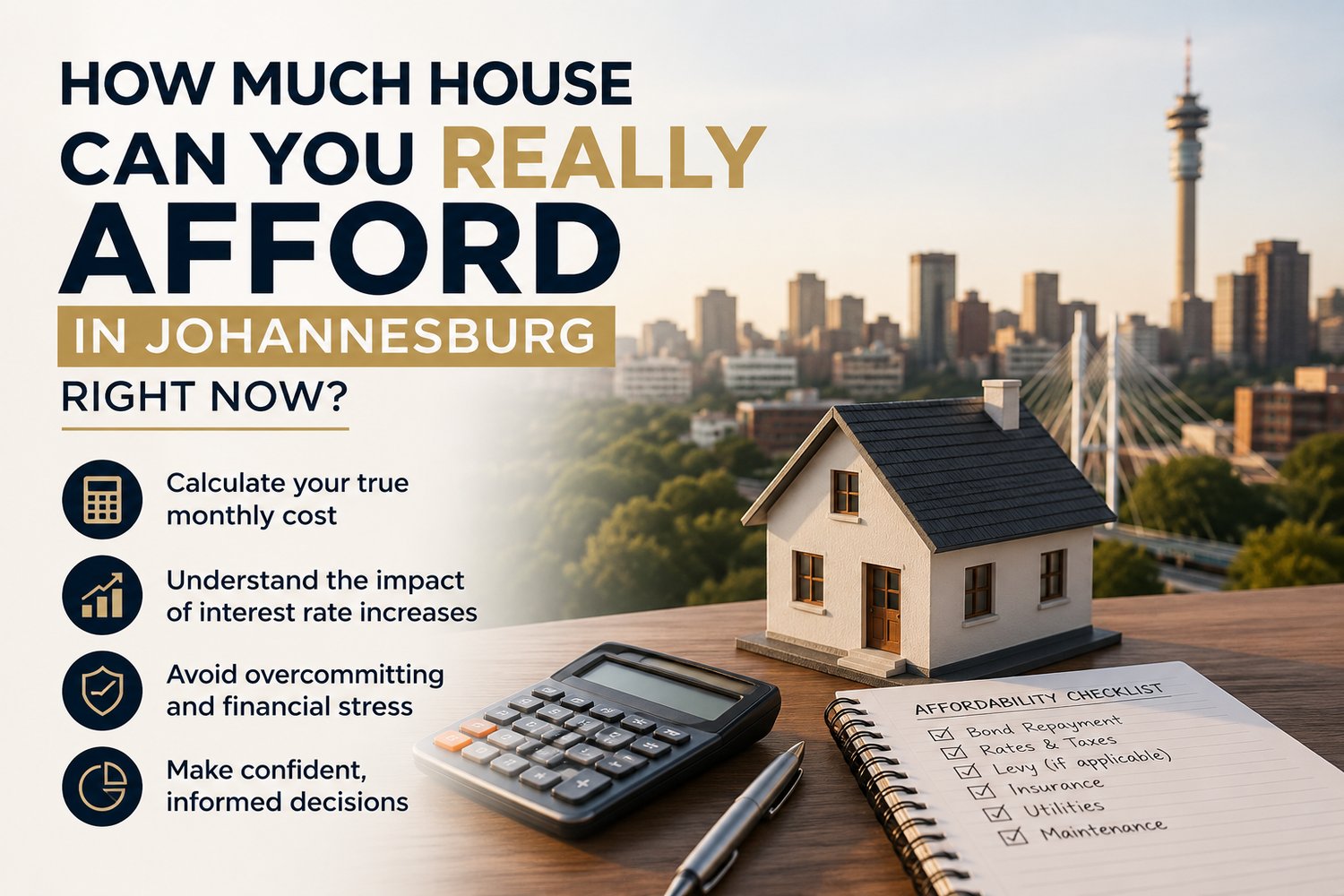

The biggest mistake is focusing only on the bond repayment.

In reality, owning property comes with additional monthly costs:

- Rates and taxes

- Levies (if applicable)

- Insurance

- Utilities

- Ongoing maintenance

When these are added, the true cost of ownership is often significantly higher than expected.

📊 A Practical Rule That Changes Everything

A useful guideline is to keep your total property costs within 25%–30% of your net income.

This gives you:

- Financial breathing room

- Flexibility if interest rates increase

- Reduced long-term pressure

⚠️ Why This Matters More Right Now

We’re currently in a market where:

- Buyers are cautious

- Sellers are under pressure

- Costs are increasing

This means the margin for error is smaller.

Buying beyond your comfort level is not just risky — it can impact your financial stability for years.

📈 The Smarter Way to Approach It

Before making an offer, take the time to understand:

- Your real monthly cost

- How rate changes affect your repayments

- Whether the purchase fits comfortably into your lifestyle

🔗 Want to Know Your Numbers?

If you want a clear, personalised view of your affordability:

👉 Use the Buyer Affordability Calculator

🧠 Final Thought

Buying property should feel like a confident decision — not a financial gamble.

The more clarity you have upfront, the better your outcome will be.