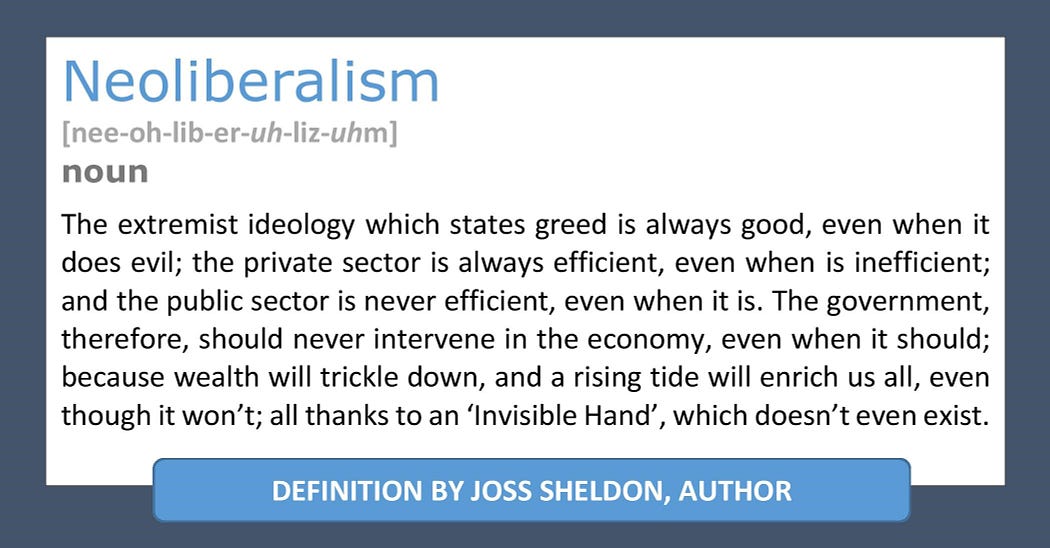

Neoliberals often claim that reducing the size of the state will create a more efficient economy, as if the existence of the state is an impediment to the free market. This ideology has been used to justify the selling off of national assets, and the scaling back of public services. But this viewpoint ignores the fact that markets rely upon states for their very existence. Without states, there can be no free markets.

(Source: Joss Sheldon)

Wherever we see people who do not live in states, people such as hunter-gatherers and tribespeople, we see a distinct lack of money and markets. Hunter-gatherers tend to hunt together and share their bounty together; they’re self-sufficient, and have no need to trade. Other stateless peoples, living in tribes and villages, also shun money. The Iroquois, for example, stockpile their produce in long houses. If a villager needs something, they approach a council of women, who listen to their appeals and then hand over the requested items. Not all stateless societies are so egalitarian, some use hierarchical structures to distribute wealth, but they all tend to do so without any money or markets.

The first record we have of money dates back to 3500BC, in Mesopotamia, where debts contracts were written on clay tablets, and deposited in palace and temple complexes (the state’s headquarters). We see similar arrangements arise with the other great states of the ancient world; in Egypt (from 2650BC) and China (from 2200BC). Such debt contracts could be passed from one person to another, like money, but there is little evidence to suggest that this happened on a regular basis. Those tablets served as a unit of account, perhaps to pay taxes, but were seldom used as a means of exchange.

Sumerian Tablets from 3500BC (Source: Wikipedia)

To see something resembling a modern economy, based on the free market, we need to skip forward a millennia or two.

The first coins we know of were made in Sardis, Western Asia, in the seventh century BC. They reached Greece within a hundred years, but were not used to buy or sell things at that time. Those coins were more like medals than modern money; stamped with the logos of aristocratic families, and given as gifts to secure alliances. Coins did not, as the neoliberals claim, evolve out of barter; they evolved out of a desire to maintain power.

The aristocratic families in Greece aspired to self-sufficiency; ruling over teams of slaves and servants, who produced everything they needed to survive. For such a family to have to resort to trade, because they were incapable of producing something themselves, was seen as a sign of failure. Gifts were exchanged, items were plundered, but exchange was almost non-existent.

Ancient coins from Sardis

This situation changed when those aristocratic Greek families united to form a state; constructing a system in which they employed magistrates, jurors and soldiers to maintain their power. As I put it in my novel, “Money Power Love”:

Those public servants needed to be paid wages. To pay those wages, taxes needed to be raised. It was agreed that they would be paid for with gold and silver coins.

The aristocratic families were forced to sell things like food and clothes, to receive those coins, so they could afford to pay their taxes. The public servants, in turn, were paid those coins, before spending them on the items the aristocratic families had been forced to sell. Markets were created and money began to flow.

Taxes forced people to buy things, sell things, and use coins.

Money Power Love (Source: Joss Sheldon)

Money Power Love (Source: Joss Sheldon)

The very instant at which the Greek state was created, was the very instant at which taxes were first raised, people were first forced to use money, and the free market was born.

The free market is not a natural phenomenon; it doesn’t arise naturally, nor does it expand naturally; it only ever comes into play when it is imposed on people by the rich and powerful.

The Greeks used their taxes to fund a huge army and navy, unlike any military force known before. State-soldiers replaced citizen-soldiers, conquered new lands, and imposed states and markets onto their new territories (where they often mined the silver and gold they needed to produce more coins).

Greece was not alone; this story repeats itself through history. In Europe, it was the Romans who took the baton from the Greeks; forming a state, and raising taxes — about three quarters of which was spent waging wars; expanding Rome’s power, and imposing markets upon vast swathes of Europe.

Coins were an essential tool for imperialistic expansion. Whereas it would have been costly to transport heavy items back to the motherland, and inefficient to transport perishable items, it made sense to sell those items for gold and silver coins, transport those coins back home, and use them to buy the items there.

This may sound like ancient history, it is, but the lesson is clear today. Without states there would be no markets; there would be no laws to protect the private ownership of land or capital, and no systems with which to protect patents or trademarks. Private businesses rely on states to educate its workforce, heal its workers, and provide infrastructure such as railways and roads.

I have not written this article to defend the existence of states. You may believe that we would be better off without them; ruling ourselves within our communities, from the bottom up. But, if this were to be the case, it would usher in the end of the free market.

No matter what the neoliberals say, states and markets are inextricably linked — you’ll struggle to maintain one without the other for any sustained period of time.

The ebook version of Money Power Love is available from this website, here.

Physical copies are available from Amazon, Barnes & Noble, Watestones, and all good online retailers…

Also in this blog series...

2. THE EVOLUTION OF MONEY: FROM GOLD COINS, TO TALLY STICKS, TO PAPER NOTES

SOURCES

1) “Debt: The First 5000 Years” by David Graber

2) “The Origins of the Market Economy: State Power, Territorial Control, and Modes of War Fighting” by Erica Schoenberger

Comments ()