Visa & Mastercard: Really Global Brands? Regional Mismatches and Strategic Consequences

On Sale

€90.00

€90.00

Short Description

Visa and Mastercard promise seamless global acceptance — but their networks don’t even share the same map. This 21-slide case study exposes how fragmented their regions and territories are, what that means for fees, compliance, and operations, and why this fragmentation opens the door to alternatives.

What’s Inside (21 slides)

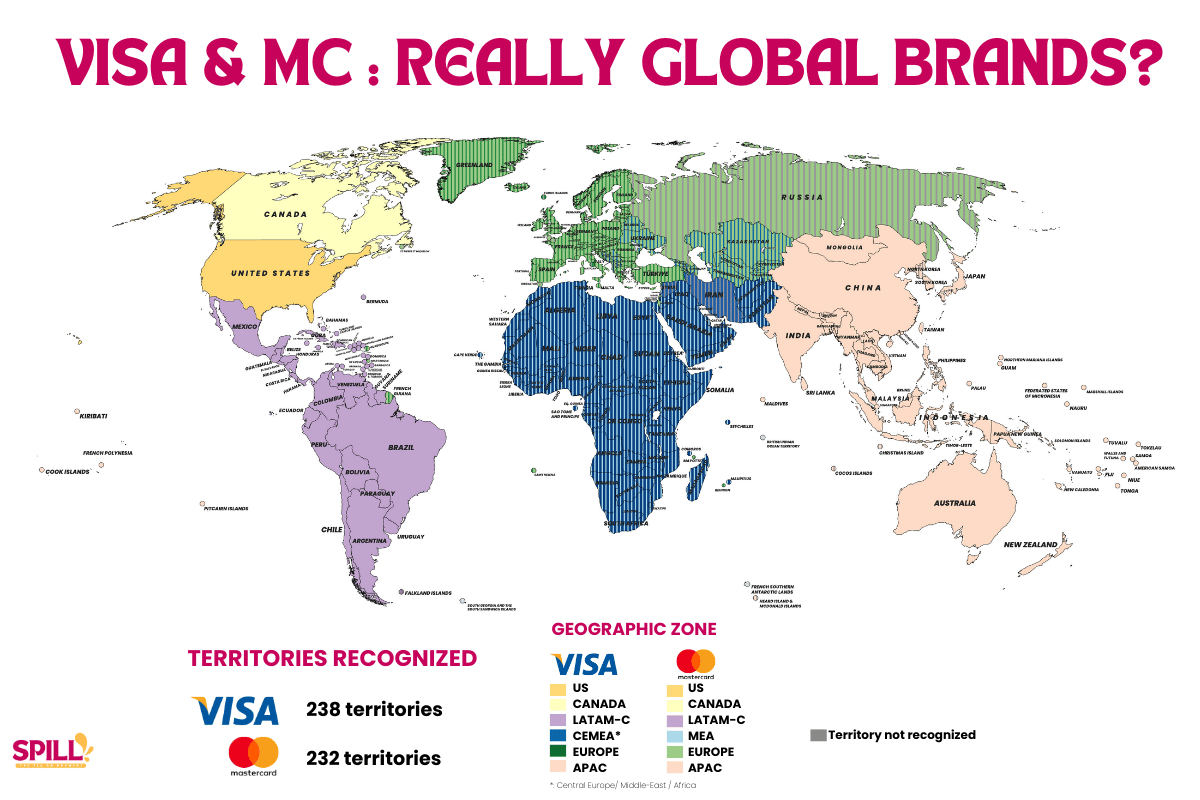

- 🌍 Global overview → Visa (238) vs Mastercard (232) territories, 25% mismatch.

- 🗺️ Regional zooms → Europe (30 mismatches), MEA (22), APAC, Americas.

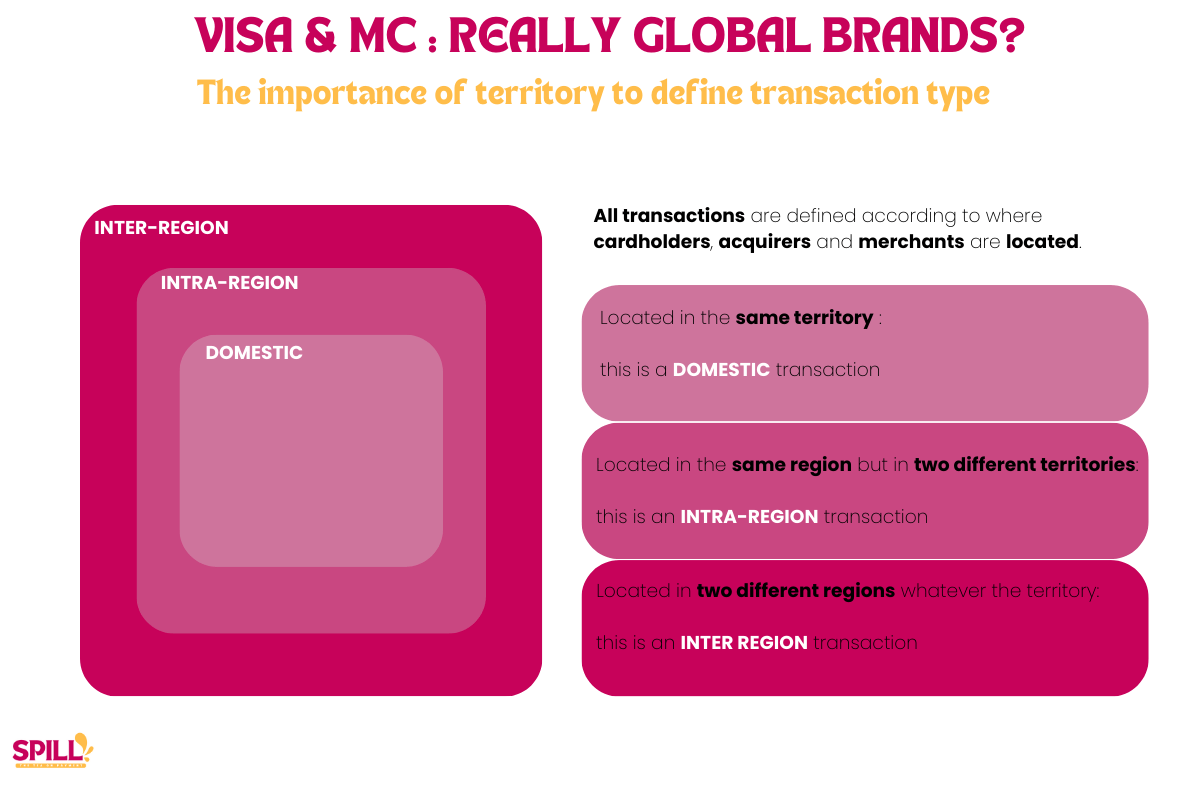

- 💸 Operational impacts → how territory definitions drive acceptance, fees, chargebacks, fraud monitoring, and compliance.

- ⚖️ Geopolitical examples → Taiwan, Russia, Iran/Syria, Vatican, and more.

- 🔄 Real transaction examples → Israel–France, Pakistan–Thailand, Georgia–Germany, Uzbekistan–China.

- 📊 Risk mapping → low/mid/high exposure by region.

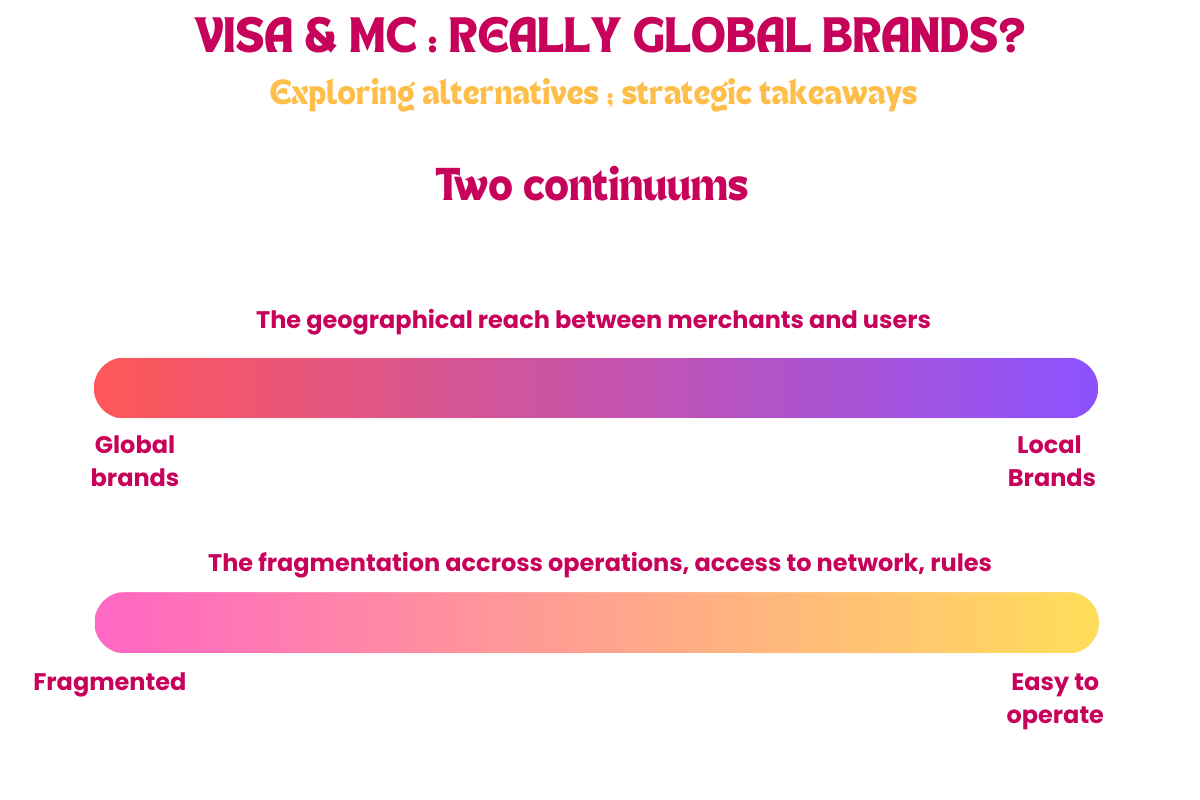

- 🏦 Strategic framing → retail networks vs infrastructures, quadrant of global/local vs simple/fragmented.

- 💡 Executive takeaways → what merchants, acquirers, and strategy teams should challenge.

Who It’s For

- Merchants negotiating acquirer contracts.

- Acquirers/PSPs explaining fees and reporting.

- Consultants and analysts need a reusable explainer.

- Strategy teams comparing global schemes with local alternatives.

Why It Matters

- Global ≠ simple → 25% of Mastercard’s map differs from Visa’s.

- Fees and compliance aren’t neutral — they depend on scheme logic, not geography.

- Alternatives gain appeal → Pix, UPI, Alipay+, and others win on clarity.

- Executive angle → this isn’t just ops detail; it’s a strategic question of dependence vs alternatives.