17 How To Master Investment and Portfolio Models

Eighteen investment and portfolio frameworks, each taught end to end — with the worked models to run them.

Eighteen investment and portfolio frameworks, each taught end to end — with the worked models to run them.

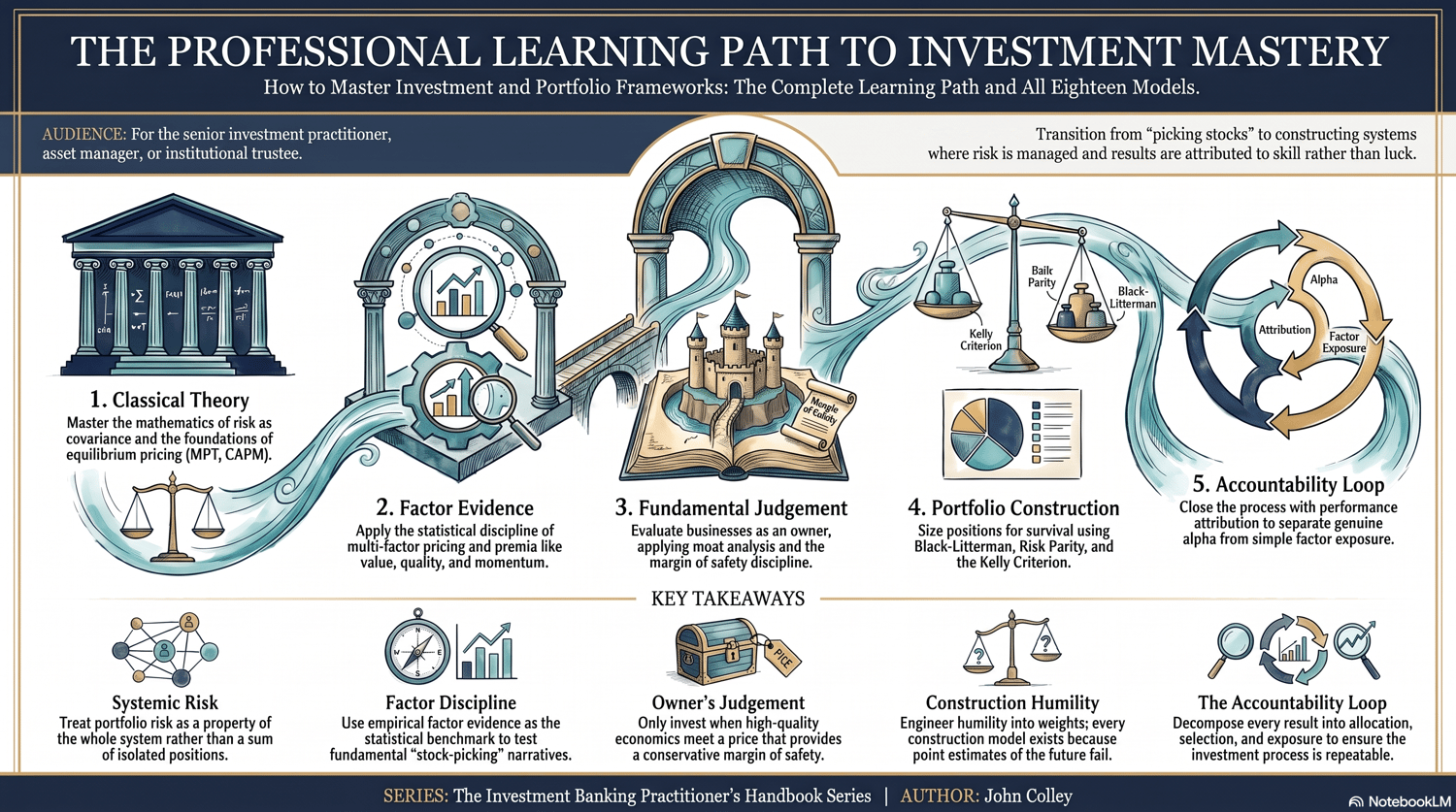

Investing well is the discipline of building a portfolio that earns the most for the risk it takes. This handbook teaches all eighteen frameworks in the Investment and Portfolio category — one chapter each — from modern portfolio theory and the pricing of risk, through the factors and value-investing lenses that pick the assets, to the position-sizing, attribution and allocation models that run the book. From Modern Portfolio Theory and the Capital Asset Pricing Model to the Kelly Criterion, the Fama-French Factor Model and Risk Parity.

What you get

The complete PDF handbook plus eighteen worked Excel models — one for every framework in the book. Blue input cells you change, formula cells that respond, and a Read-me tab on each, so you can run the numbers on your own assumptions.

How every chapter is built

Read one and you can build any. Each framework follows the same thirteen-section rhythm: the question it answers, what it is, who uses it, its anatomy, inputs and outputs, how to build it step by step, a worked example, strengths, limits and pitfalls, industry notes, how it connects to the other frameworks, modern relevance, using AI on it, and a practitioner’s checklist.

The eighteen frameworks

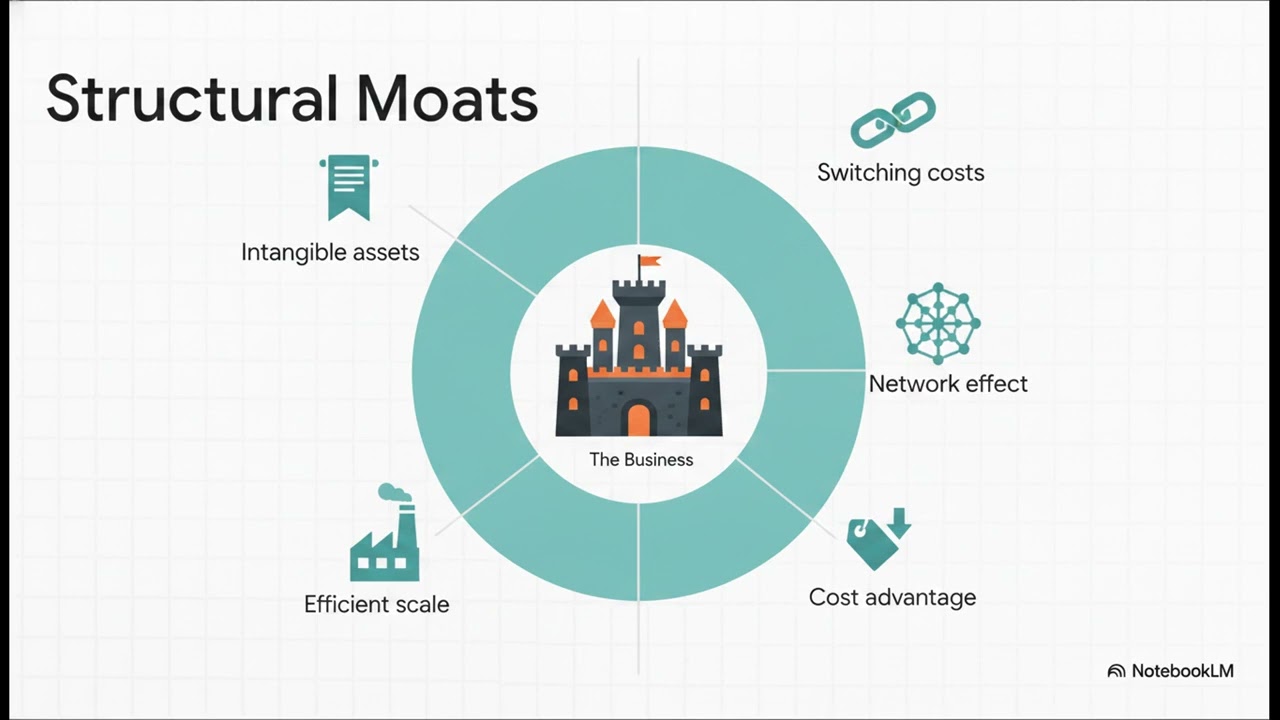

Modern Portfolio Theory, the Efficient Frontier, the Capital Asset Pricing Model, the Value Factor, the Quality Factor, the Momentum Factor, the Buffett-Munger Framework, the Margin of Safety, Moat Analysis, the Position Sizing Model, the Kelly Criterion, Risk-Adjusted Return, the Investment Scorecard, Performance Attribution, Arbitrage Pricing Theory, the Fama-French Factor Model, the Black-Litterman Model and Risk Parity.

The learning path

The chapters are ordered as a single connected build, not an alphabetical list — from portfolio theory and the pricing of risk, through the factors and value lenses that pick assets, to the sizing, attribution and allocation models that run the book.

Who it’s for

Portfolio managers, analysts, wealth advisers and serious private investors who must choose assets, size positions and defend the risk-adjusted return.

How to use it

Work straight through to master the category, or jump to a single framework when you need it for live work.

Book 17 of the Business Framework Library, part of The Investment Banking Practitioner’s Handbook Series. Master this category on its own, or reach for the Business Framework Compendium when you want the one-page reference to all 467 frameworks.

By John Colley — Cambridge University MA · MBA with Distinction, Bayes Business School · 30+ years in investment banking, M&A and private equity.