TS-ParamScape Suite_2.0

ParamScape 2.0

ParamScape3D and ParamScapeRank

Works with TradeStation and MultiCharts!

Paramscape 3D-SingleLineCollapse

Update Summer 2026: TS-ParamScape Suite Upgrade

The TS-ParamScape tools have received a major Summer 2026 upgrade.

TS-ParamScape3D now features a refreshed user interface, improved workflow, and enhanced visual analysis tools, including a new water-level view and heatmap-style parameter surface display. These additions make it easier to see where parameter performance is stable, where it breaks down, and where the optimization surface may be too fragile.

TS-ParamScapeRank has taken an even bigger leap forward. The upgraded Rank analysis provides a much deeper and more practical view of parameter importance, helping traders better understand which inputs truly matter and which may be curve-fit noise. This is a quantum leap over the older workflow and makes the tool far more useful for evaluating optimization robustness.

Together, TS-ParamScape3D and TS-ParamScapeRank help TradeStation strategy developers move beyond simple “best parameter” thinking and toward a more complete understanding of parameter sensitivity, surface stability, and optimization quality.

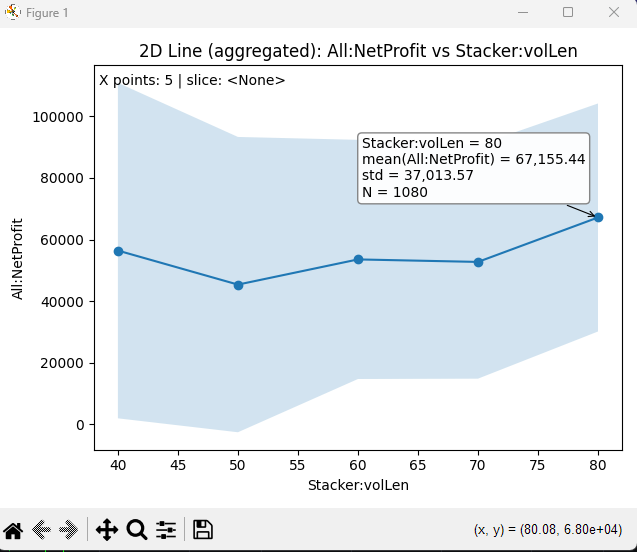

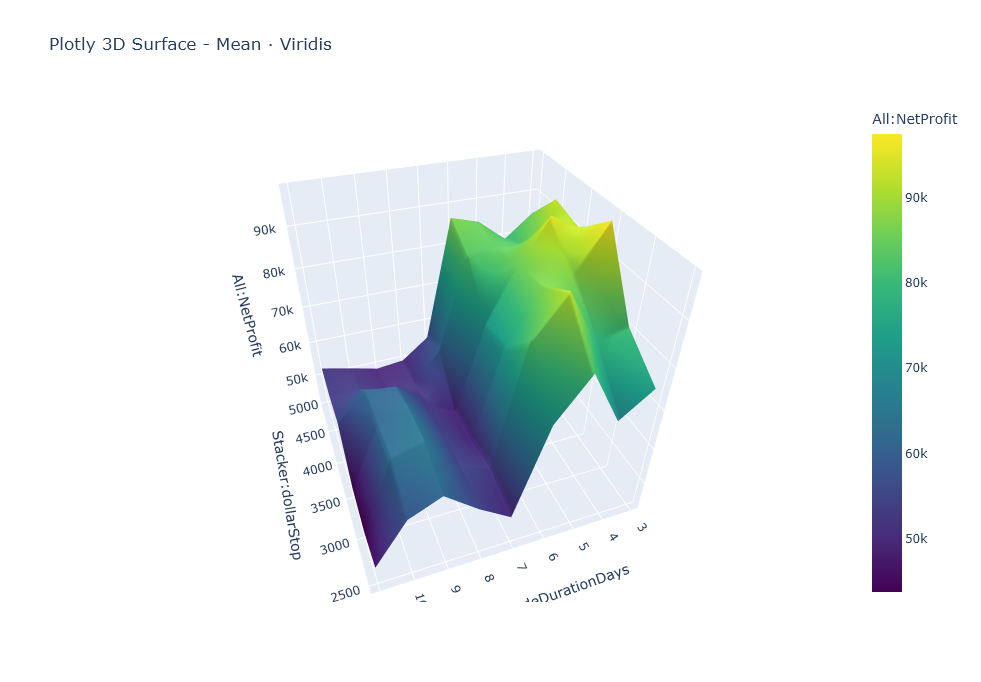

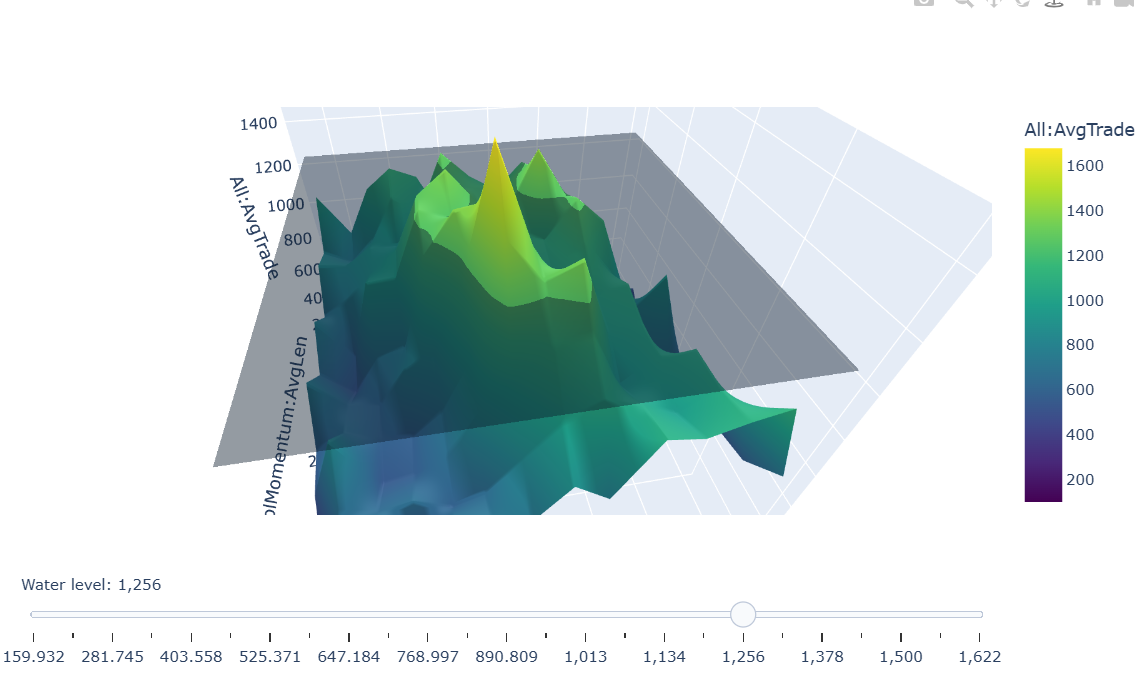

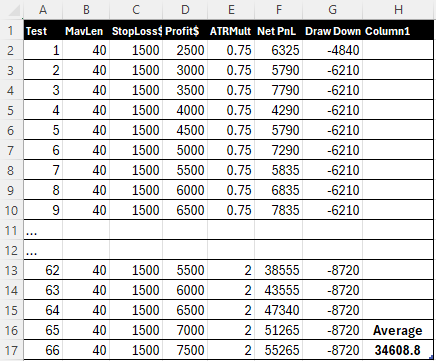

Plotting just the results of just two parameters is relatively straight forward. However, plotting optimzations of three or more is quite a bit more complicated. With this tool, we can plot two of N parameters against several objective functions. Below is a chart of moving average length versus stop loss dollars. The Z-Axis this time is the mean or average of all the addresses the contain the X and Y parameters. Take a look at this table.

Across 66 parameter combinations with Mav Len fixed at 40 and StopLoss$ fixed at 1500, the average result represents the overall performance of this setting. This average reflects how the strategy behaves under different values of Profit$ and ATRMult, giving a broader sense of robustness. If you locate the point X = 40 and Y = 1500 on the figure you will see the 34608 mean value. If a point on the surface is high and surrounded

You can further smooth the surface by averaging each point with its 3 × 3 neighborhood. This reduces noise and produces a smoother contour. Sharp or brittle spikes in the mean surface will still stand out, while broad high regions will appear even more clearly as plateaus.

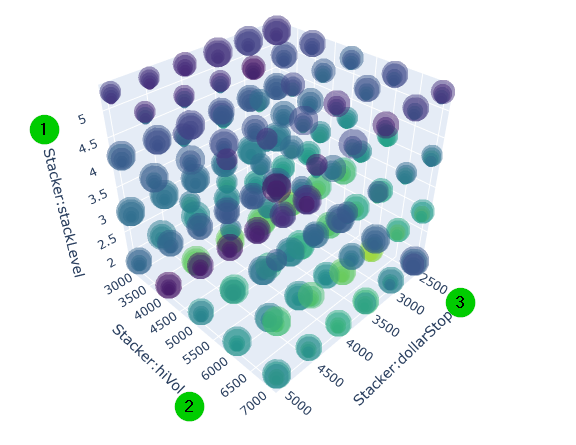

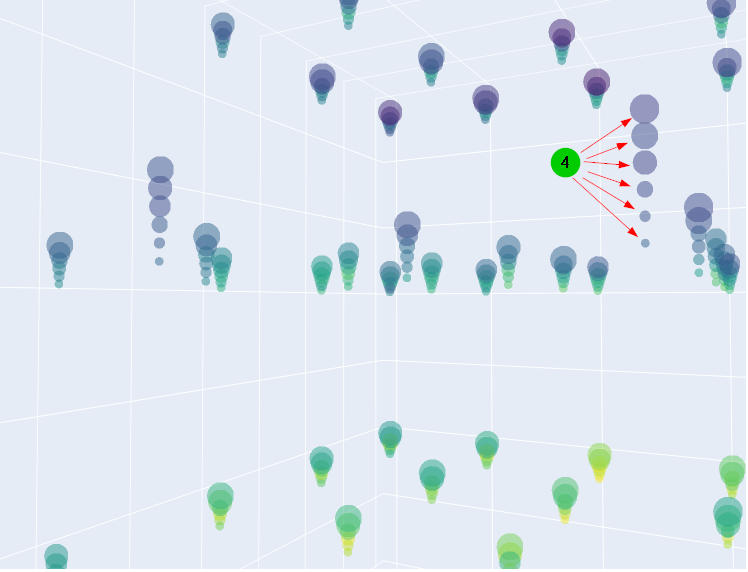

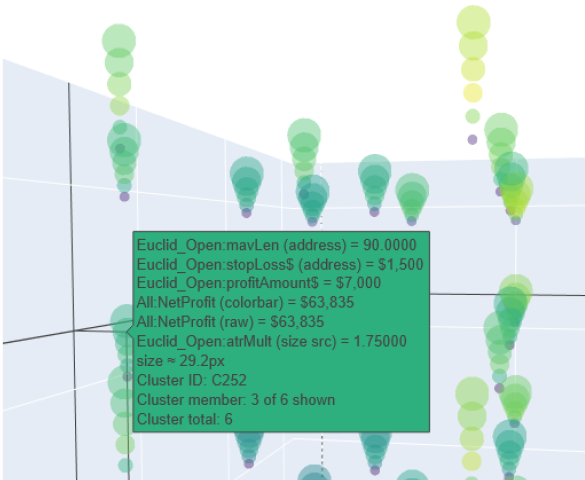

How to read the Volumetric Plot

Each dot is one backtest run at (MA length, Stop loss, Profit objective, ATR multiple) .

Turn on De-stack (Z-only “raindrop”) to separate overlapping results that share the same X and Y—clusters become vertical “inverted raindrops.” These multiple values are "jittered" by small offsets of the Z axis.

Hover any dot to see the exact (non-jittered) values. What does the volumetric de-stacked chart show you? You can zoom into the cloud and find the values that show the highest NetProfit and examine those values across the fourth parameter - in this case the average true range multiplier.

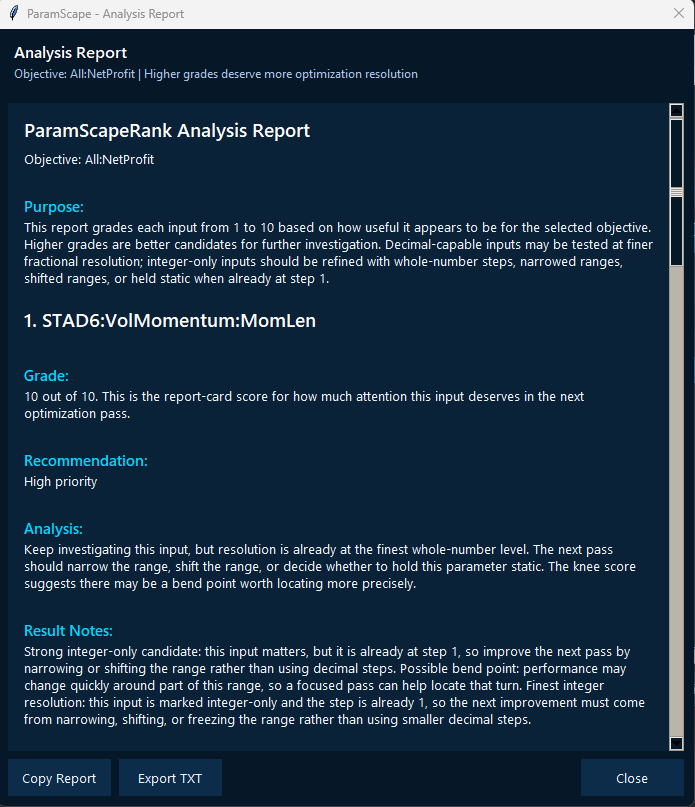

Ranking Importance of Inputs Across Optimization Space

What this tool does (in one breath)

TS-ParamScapeRank reads a tab-delimited optimization file and tells you: Which parameters matter most (ranking), Whether they have a forgiving “plateau” or a sharp “knee” (diminishing returns), And gives ready-to-run ranges and grid steps for a focused re-optimization. It’s built for traders, not statisticians. The outputs are “what it means” and “what to do next.”

Suggest Search Space Ranges and WHY!

Chat GPT Response

Summary by parameter

1) dollarStop — robust and not very important

- Elite range: 2500–5000, step 500, suggested start 4000.

- Sensitivity = 0.09 (low) and Trend = flat.

- Interpretation: within the elite zone, performance doesn’t consistently get better or worse as you change the stop, and the system isn’t very sensitive to it.

- Takeaway: choose a reasonable value (e.g., 4000) for risk control and leave it alone; don’t over-optimize it.

2) hiVol — moderately important, better higher

- Elite range: 3000–7000, step 1000, suggested start 6000.

- Sensitivity = 0.30 (moderate) and Trend = increasing.

- Interpretation: higher hiVol values tend to correspond to better results in the elite slice.

- Takeaway: this is a meaningful lever; if you must bias, bias toward the upper end (6000–7000).

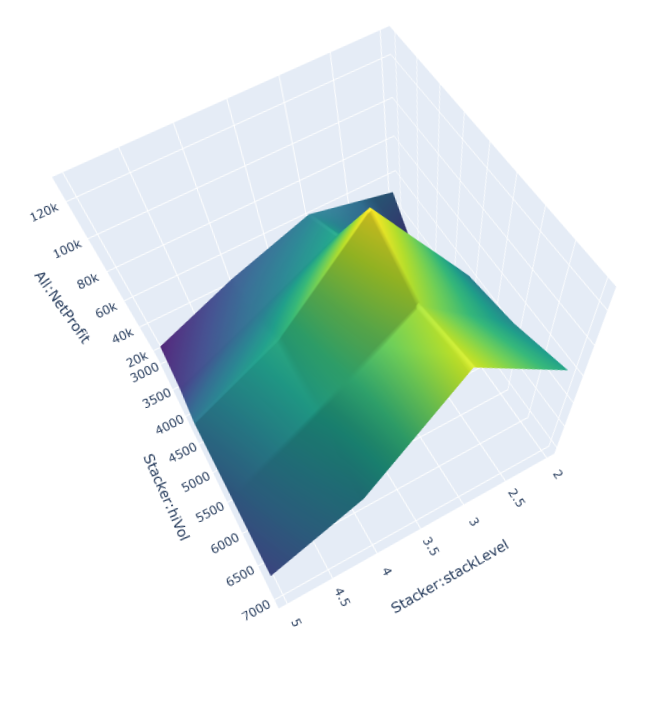

3) stackLevel — meaningful lever, better lower

- Elite range: 2–5 in steps of 1, suggested start 3.

- Sensitivity = 0.46 (fairly high) and Trend = decreasing.

- Interpretation: as stacking increases, results tend to deteriorate; lower stack levels perform better among the elite runs.

- Takeaway: keep stacking conservative—2–3 looks like the robust neighborhood.

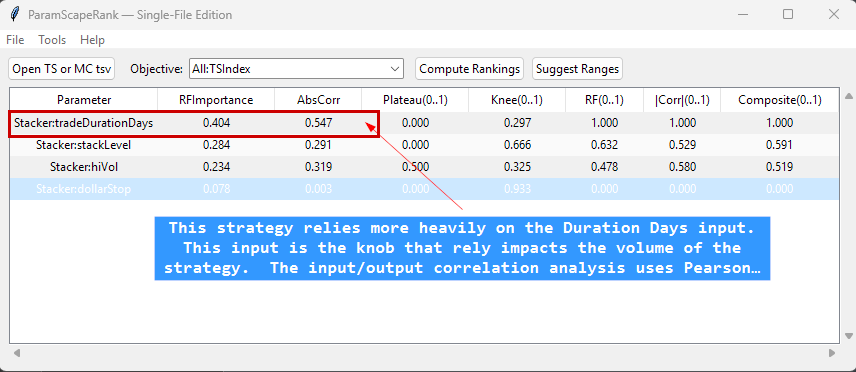

4) tradeDurationDays — most influential of the set, better shorter

- Elite range: 3–8 in steps of 1, suggested start 4.

- Sensitivity = 0.56 (highest here) and Trend = decreasing.

- Interpretation: shorter duration settings tend to work better, and performance is quite sensitive to this knob.

- Takeaway: treat this as a primary tuning parameter; 3–4 days is the “safe/strong” area suggested by the elite runs.

Overall “story”

Among the top-performing solutions, the system seems to prefer:

- shorter trade durations (strongest effect),

- less stacking (important effect),

- higher hiVol thresholds (moderate effect),

- while dollarStop is mostly a robustness/risk-control setting with little directional edge inside the elite zone.

That’s exactly the kind of output you want: it separates “true performance drivers” from “settings that mainly shape risk but don’t move the needle much.”