IRS CP297 Final Notice of Intent to Levy (Business) Response Kit

What Is CP297?

CP297 is a Final Notice of Intent to Levy issued to businesses. It signals that the IRS has assessed the tax and may proceed with enforced collection if no timely action is taken.

This is a final-stage collection notice.

After the 30-day window expires, the IRS may levy:

• Business bank accounts

• Accounts receivable

• Equipment and business assets

• Potentially pursue responsible officers for trust fund liabilities

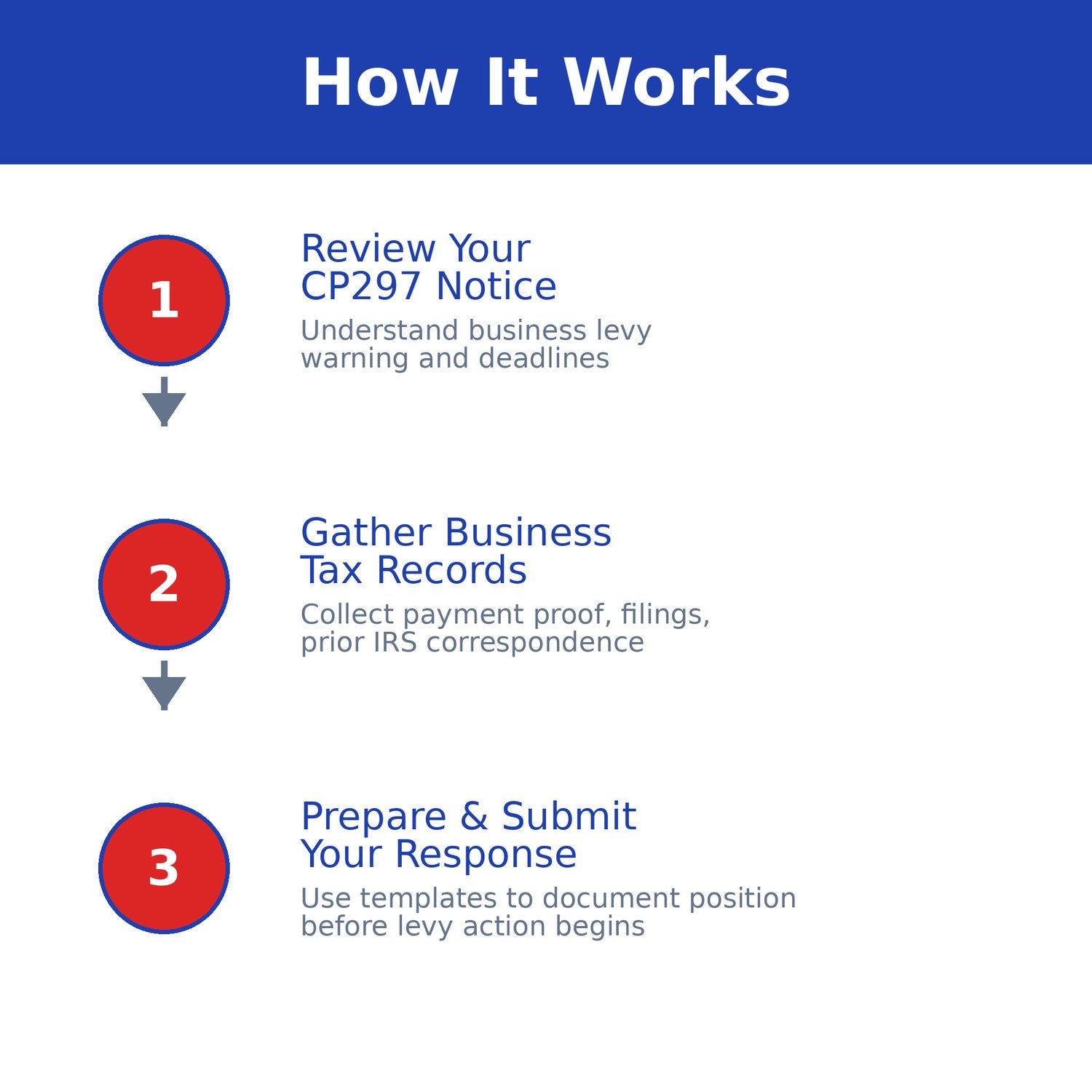

You generally have 30 days from the date of the notice to request a Collection Due Process (CDP) hearing to preserve full appeal rights.

Who This Is For

• Corporations, LLCs, partnerships with tax debt

• Businesses with payroll tax liabilities

• Owners who received CP297

• Responsible parties concerned about enforcement exposure

Who This Is Not For

• Individuals who received CP90 or LT11

• Early balance-due notices (CP14 / CP501 / CP503)

• CP504 state refund levy notices

What This Documentation System Helps You Do

• Preserve CDP hearing rights

• Organize financial records

• Document asset exposure

• Structure communication records

• Prepare documentation before enforcement escalates

This system provides structured templates and documentation tools to help you respond in an organized, professional manner.

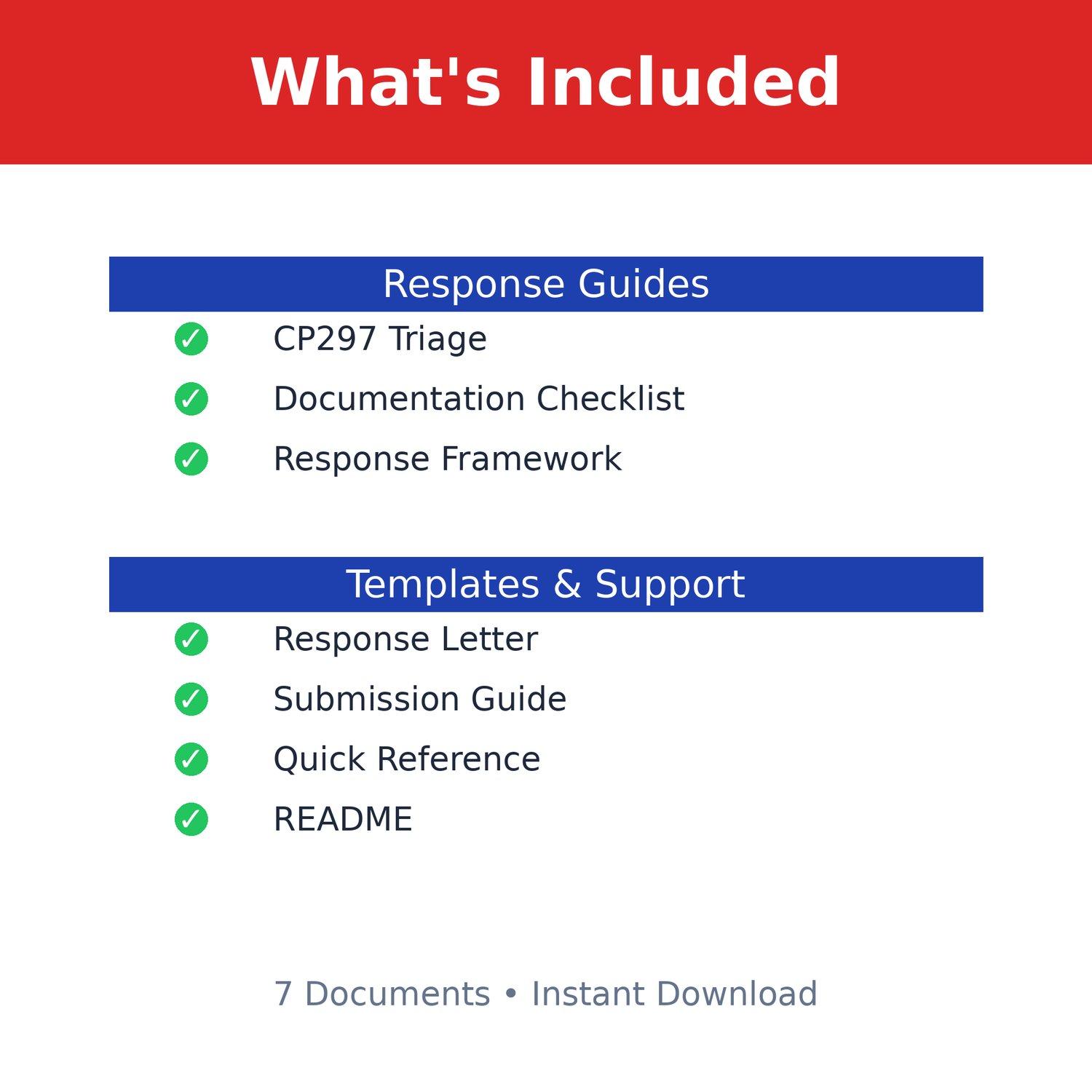

What’s Included

• CP297 Response Planning Framework

• CDP Hearing Documentation Organizer

• Business Asset & Receivables Worksheet

• Responsible Officer Exposure Review Template

• IRS Communication Log

• Deadline Tracking Sheet

• Submission Checklist

Delivered as digital documentation templates.

Important Notice

This product provides documentation templates and organizational tools.

It is not legal advice, tax advice, or representation.

Consult qualified professionals for legal or tax-specific guidance.

FAQ

How long do I have to respond to CP297?

You generally have 30 days to request a Collection Due Process hearing to preserve full appeal rights.

Can the IRS levy my business bank account?

Yes. After the final notice period expires, the IRS may levy business accounts and receivables.

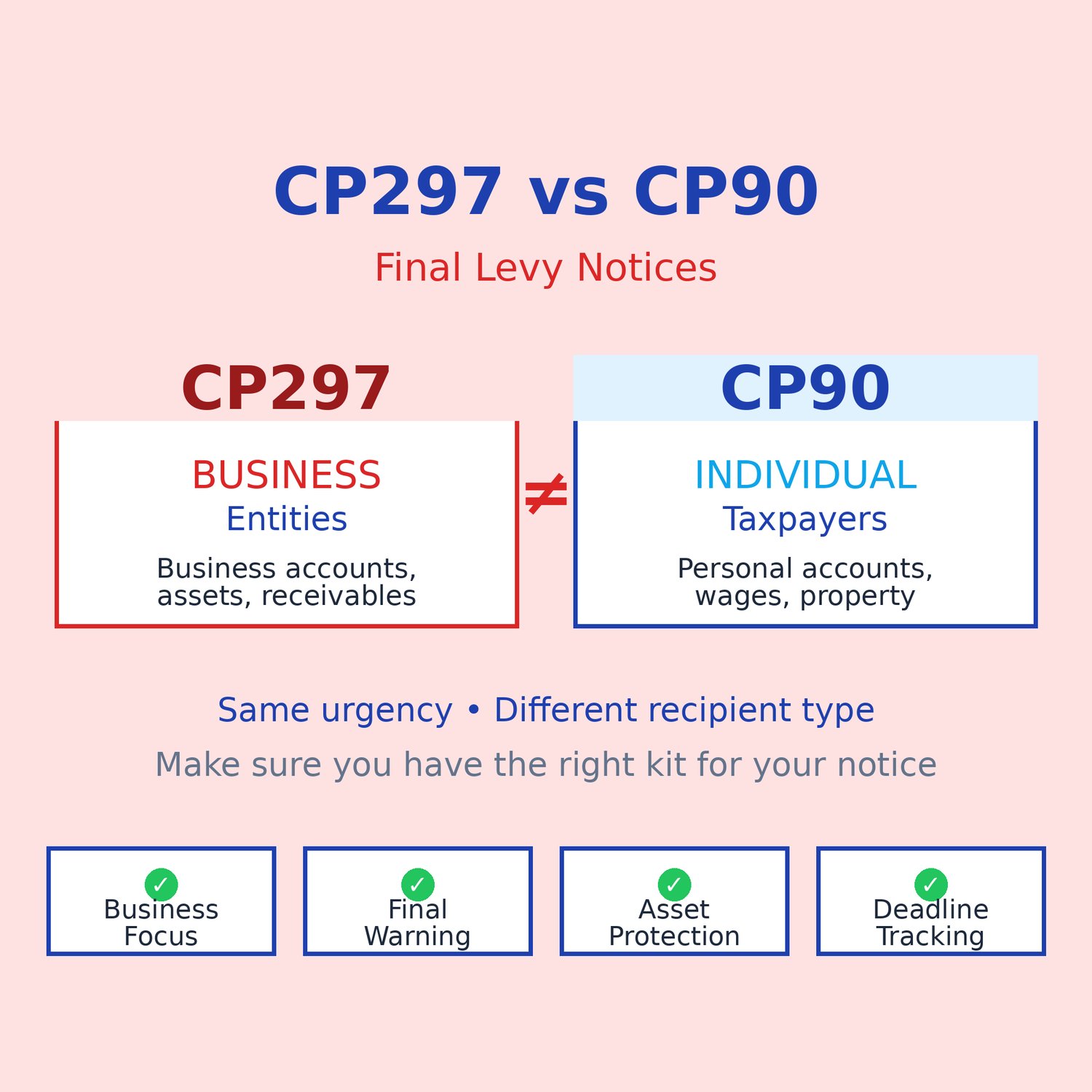

Is CP297 the same as CP90?

No. CP297 is issued to businesses. CP90 is issued to individuals.

Does this include guidance for Form 12153?

Yes. The system includes documentation support related to CDP hearing requests.

Is this legal representation?

No. This is a documentation system designed to help you organize and respond.