F1 What is so special about Itô increments

On Sale

£0.00

Pay what you want:

£

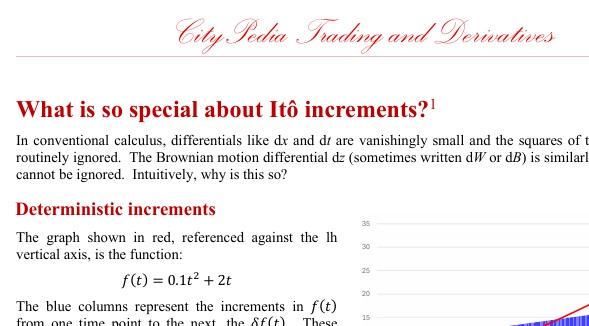

In conventional calculus, differentials like dx and dt are vanishingly small and the squares of these differentials are routinely ignored. The Brownian motion differential dz (sometimes written dW or dB) is similarly small but its square cannot be ignored. Intuitively, why is this so?