A single late payment can follow you for years. It sits on your credit report, quietly dragging down your score and costing you money on every loan, credit card, and mortgage application you submit. What most people do not know is that you can ask the creditor to remove it — politely, professionally, and completely within your rights.

That request is called a goodwill letter. And when it works — which it does more often than most people expect — it can remove an accurate negative mark from your credit report without a dispute, without legal action, and without paying a credit repair company hundreds of dollars a month.

This guide explains exactly what a goodwill letter is, when to send one, who to send it to, what to write, and what to expect. At the bottom you will find three free templates you can download and use today.

QUICK ANSWER

A goodwill letter is a written request to a creditor asking them to remove a negative mark — usually a late payment — from your credit report as a courtesy. It is not a dispute. You are acknowledging the late payment happened and asking the creditor to remove it anyway based on your overall payment history and the circumstances that caused the issue.

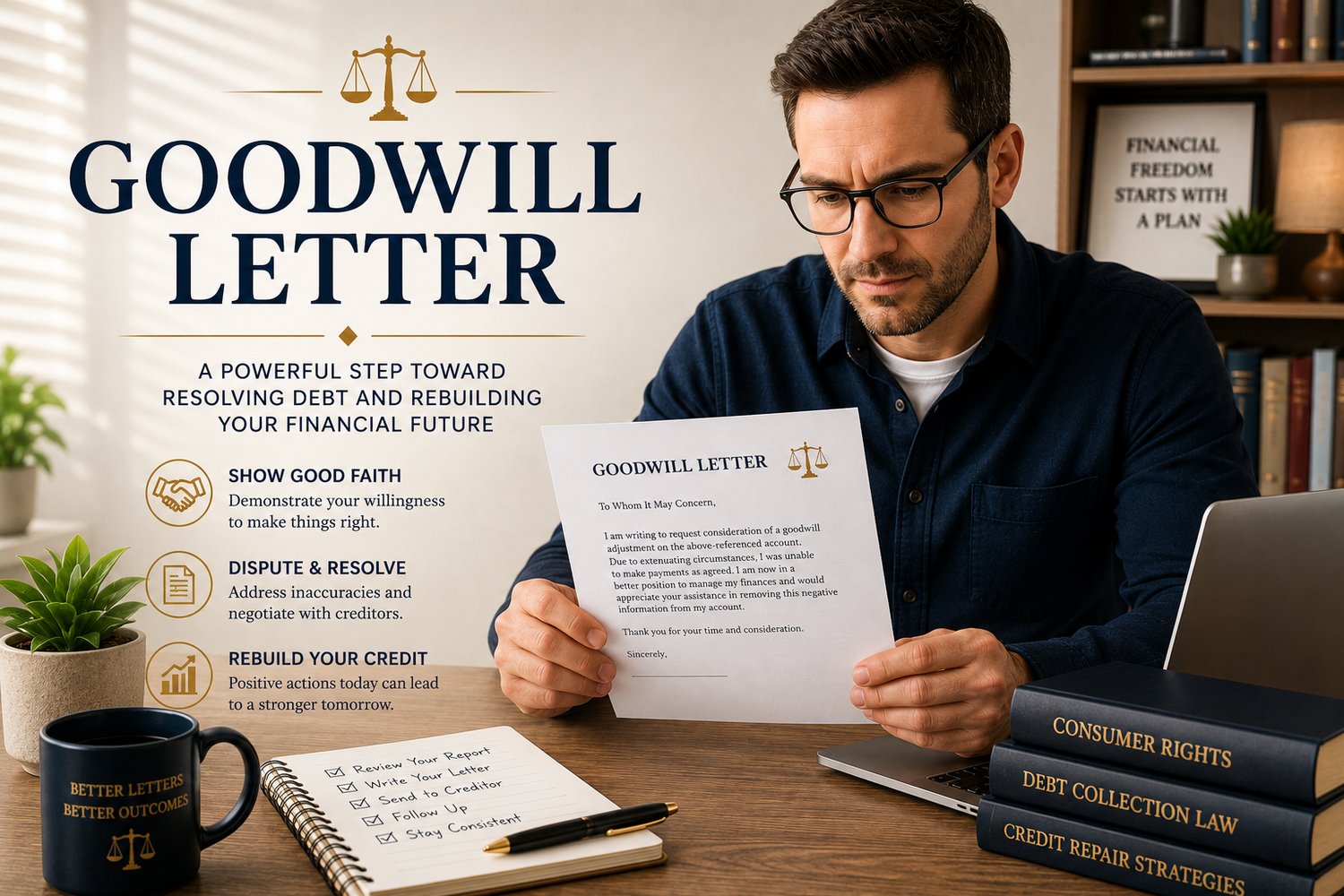

What Is a Goodwill Letter?

A goodwill letter is a formal written appeal to a creditor or lender asking them to remove a negative item from your credit report as a gesture of goodwill. Unlike a credit dispute — which challenges the accuracy of information — a goodwill letter acknowledges that the negative mark is accurate and appeals to the creditor's discretion to remove it anyway.

Creditors are not legally required to honor goodwill requests. But many do — especially when the customer has an otherwise strong payment history, the late payment was isolated and out of character, the account is currently in good standing, and the letter is personal, honest, and well written.

This surprises people. But it makes business sense from the creditor's perspective. If you have been a reliable customer for years and had one slip — a medical emergency, a job loss, a billing mix-up — removing that mark costs them nothing and keeps a good customer loyal. That is the leverage you are working with.

Goodwill Letter vs Credit Dispute — What Is the Difference?

- Used for accurate negative marks

- Used for inaccurate or unverifiable information

- Appeals to creditor's discretion

- Invokes your legal rights under the FCRA

- No legal obligation for creditor to comply

- Creditor must investigate and respond within 30 days

- Works best on isolated late payments

- Works on errors, fraud, and unverifiable accounts

- Sent directly to the creditor

- Sent to the credit bureau or creditor as furnisher

- Success depends on relationship and tone

- Success depends on proof and documentation

When Does a Goodwill Letter Work?

Goodwill letters work best in specific situations. Understanding when to send one — and when not to — is the difference between a request that gets honored and one that gets ignored.

Most likely to succeed:

• The late payment was isolated — one or two instances on an otherwise spotless record

• The account is currently in good standing and you have been paying on time since

• You have a legitimate reason for the late payment — medical emergency, job loss, natural disaster, billing error, or family hardship

• You have been a customer of this creditor for a significant period of time

• The late payment is recent enough that the creditor still has the account — not a collection agency

Less likely to succeed:

• Multiple late payments on the same account showing a pattern of non-payment

• The account was sent to collections or charged off

• You have no history with the creditor beyond the delinquent account

• You are currently behind on the account you are writing about

• The late payment was recent with no subsequent positive history to point to

IMPORTANT: A goodwill letter is not a dispute. Do not claim the information is inaccurate if it is not. That is a false dispute and can backfire, making it harder to remove the item later.

Who to Send a Goodwill Letter To

This is where many people go wrong. A goodwill letter goes to the original creditor — not the credit bureau. The credit bureau only reports what the creditor tells them. The creditor is the one with the authority to update or remove the negative mark.

Send your letter to the creditor's customer service address or, better yet, their executive resolution team. The executive office handles escalated customer concerns and has more authority to act on goodwill requests than a standard customer service representative.

How to find the right address:

• Check your original account statement or the creditor's website under the Contact or Customer Service section

• Call the creditor's customer service line and ask for the mailing address for the executive resolution or executive customer service team

• Search the creditor name plus "executive office address" or "goodwill letter address" — many are publicly documented

• Send via USPS Certified Mail with Return Receipt Requested so you have proof of delivery

How to Write a Goodwill Letter — Step by Step

A goodwill letter has one job: to make a creditor want to help you. That means it needs to be personal, honest, concise, and respectful. Generic templates that sound like they were copied from the internet get ignored. A letter that sounds like a real person explaining a real situation gets read.

Here is the structure that works:

Step 1 — Open with who you are and your account history

Identify yourself, your account number, and how long you have been a customer. Lead with the positive. If you have been a customer for seven years with a perfect payment history outside of one incident, say that in the first two sentences. You are establishing your credibility before you make your ask.

Step 2 — Acknowledge the late payment honestly

Do not make excuses. Do not claim the information is wrong. Acknowledge that the late payment happened and take responsibility for it. Creditors respond better to honesty than to deflection. One clear sentence: "I am aware that my payment due on [date] was received late, and I take full responsibility for that."

Step 3 — Explain the circumstances briefly

Give one honest reason for the late payment — a medical emergency, a job loss, a family crisis, a billing mix-up, a period of financial hardship. Keep it to two or three sentences. You are not asking for sympathy. You are providing context that explains why an otherwise reliable customer had a single lapse.

Step 4 — Show what has changed

Demonstrate that the circumstances have been resolved and that you have returned to on-time payment. Point to your payment history since the incident. If you have made twelve consecutive on-time payments since the late one, say that specifically. Concrete evidence is more persuasive than general assurances.

Step 5 — Make the specific ask

Be direct and specific. Ask the creditor to remove the negative mark from your credit report as a courtesy. Do not demand. Do not threaten. Simply ask — clearly and politely. "I am respectfully requesting that you consider removing the late payment notation from my credit report as a goodwill adjustment."

Step 6 — Close with appreciation

Thank the creditor for their time and consideration. Express that you value the relationship and intend to remain a loyal customer. Keep it brief. One or two sentences is enough. Sign with your full name, account number, and contact information.

WHAT TO AVOID IN YOUR GOODWILL LETTER

• Do not threaten legal action — this is a goodwill request, not a legal demand

• Do not claim the information is inaccurate if it is accurate

• Do not send the letter to the credit bureau — send it to the creditor

• Do not use a generic template that sounds copied — personalize every letter

• Do not write a long, emotional letter — keep it under one page

• Do not give up after one rejection — send to a different department or try again in 60 days

3 Free Goodwill Letter Templates

Below are three goodwill letter templates for the most common situations. Each one is written to be personal, professional, and persuasive. Replace the bracketed fields with your own information before sending.

GET THE COMPLETE TEMPLATE BUNDLE FREE

Download all 3 templates as a formatted PDF — ready to fill in and send today. Enter your email below and we will send them directly to your inbox.

After downloading, visit our Templates page to get the complete Goodwill Letter Bundle — 5 professional versions for $15.

Template 1 — General Late Payment (Most Common)

Use this version for a standard late payment on a credit card, personal loan, or retail account where you had a temporary hardship.

[YOUR FULL NAME]

[YOUR ADDRESS]

[CITY, STATE, ZIP]

[DATE]

[CREDITOR NAME]

[CREDITOR ADDRESS]

[CITY, STATE, ZIP]

Re: Goodwill Adjustment Request — Account Number [ACCOUNT NUMBER]

Dear [CREDITOR NAME] Customer Relations Team,

I am writing to request a goodwill adjustment on my account. I have been a customer with [CREDITOR NAME] since [YEAR] and have maintained a consistent record of on-time payments throughout our relationship. I value this account and take pride in my payment history.

I am aware that a late payment was recorded on my account on [DATE OF LATE PAYMENT], and I take full responsibility for it. At that time, I was experiencing [BRIEF DESCRIPTION OF HARDSHIP — e.g., a medical emergency, unexpected job loss, family crisis]. This was an isolated situation that has since been fully resolved.

Since that time, I have made [NUMBER] consecutive on-time payments and have returned to the consistent payment behavior that has defined my account history. I am committed to maintaining that record going forward.

I am respectfully requesting that you consider removing the late payment notation from my credit report as a goodwill adjustment. I understand this is entirely at your discretion and I genuinely appreciate you taking the time to review my request.

Thank you for your consideration. I look forward to continuing my relationship with [CREDITOR NAME] for many years to come.

Sincerely,

[YOUR FULL NAME]

Account Number: [ACCOUNT NUMBER]

Phone: [PHONE NUMBER]

Template 2 — Medical Emergency Late Payment

Use this version specifically when the late payment was caused by a medical situation — illness, hospitalization, or unexpected medical bills. Medical hardship is one of the strongest grounds for a goodwill request.

[YOUR FULL NAME]

[YOUR ADDRESS]

[CITY, STATE, ZIP]

[DATE]

[CREDITOR NAME] · [CREDITOR ADDRESS]

Re: Goodwill Adjustment Request — Medical Hardship — Account [ACCOUNT NUMBER]

Dear [CREDITOR NAME] Customer Relations Team,

My name is [YOUR NAME] and I am writing to respectfully request a goodwill adjustment on my account number [ACCOUNT NUMBER]. I have been a customer since [YEAR] and have maintained an on-time payment record that I am proud of.

In [MONTH/YEAR], I experienced a serious medical situation — [BRIEF DESCRIPTION, e.g., an unexpected hospitalization, a surgical emergency, a significant illness] — that required my immediate and full attention. During that period, my finances were disrupted in ways I could not have anticipated, and I was unable to make my payment on time. I take full responsibility for the late payment that resulted.

I have since fully recovered and have made every payment on time since [DATE OF FIRST ON-TIME PAYMENT AFTER LATE]. I have [NUMBER] consecutive on-time payments on this account and intend to maintain that record going forward.

Medical hardships are by nature unexpected. They do not reflect how I manage my finances or my commitment to my obligations. I am requesting that you consider removing the late payment from my credit report as a goodwill gesture, in recognition of my overall history as a reliable customer.

I sincerely appreciate your time and consideration.

Sincerely,

[YOUR FULL NAME]

Account: [ACCOUNT NUMBER]

Phone: [PHONE]

Template 3 — Billing Error or Missed Notification

Use this version when the late payment resulted from a billing error, a payment that was not properly applied, a notification you did not receive, or an autopay failure — situations where the fault is at least partially administrative rather than personal financial hardship.

[YOUR FULL NAME]

[YOUR ADDRESS]

[DATE]

[CREDITOR NAME]

[CREDITOR ADDRESS]

Re: Goodwill Adjustment Request — Account [ACCOUNT NUMBER]

Dear [CREDITOR NAME] Customer Relations Team,

I am [YOUR NAME], a [CREDITOR NAME] customer since [YEAR]. I am writing to request a goodwill adjustment for a late payment recorded on my account in [MONTH/YEAR].

The late payment in question occurred due to [BRIEF DESCRIPTION — e.g., an autopay failure I was unaware of, a billing statement that was not received at my updated address, a payment processing error]. As soon as I became aware of the issue, I resolved it immediately. I want to be transparent: I acknowledge that the payment was ultimately late regardless of the circumstances, and I take responsibility for not catching it sooner.

Prior to this incident, I had maintained a perfect payment history with [CREDITOR NAME]. Since resolving the issue, I have made [NUMBER] consecutive on-time payments and have put additional measures in place to ensure this does not happen again.

I respectfully request that you remove this late payment from my credit report as a goodwill adjustment. This one mark does not reflect the payment relationship I have worked to maintain with [CREDITOR NAME] over the years.

Thank you for your time and for considering my request.

Sincerely,

[YOUR FULL NAME]

Account: [ACCOUNT NUMBER]

Phone: [PHONE]

What Happens After You Send a Goodwill Letter?

Most creditors respond within 2 to 6 weeks. Here are the four possible outcomes and what to do in each case:

1. They agree and remove the late payment

The best outcome. You will receive written confirmation, and the change will appear on your credit report within 30 to 60 days. Pull your credit report to confirm the deletion and check all three bureaus — Equifax, Experian, and TransUnion — since not all creditors report to all three.

2. They decline

A decline is not the end. Wait 60 days and send a new letter to a different contact — the executive resolution team, the CEO's office, or a different department. Many consumers have success on a second or third attempt. You can also try calling and asking to speak with someone in the executive customer relations team directly.

3. They do not respond

If you sent via certified mail and received confirmation of delivery, follow up in writing after 30 days. Reference your original letter and the certified mail tracking number. A second letter sent to a more senior contact often gets a response where the first did not.

4. They partially adjust the reporting

Some creditors will not delete the late payment but will update the account status or add a comment to the record. This is less valuable than full removal but can still improve how lenders view the account. If this happens, continue sending letters requesting full removal.

Frequently Asked Questions

Does a goodwill letter actually work?

Yes — more often than most people expect. Success rates vary by creditor and by the strength of your letter, but consumers with strong overall payment histories and isolated late payments frequently receive goodwill removals. Capital One, Bank of America, and many credit unions have documented histories of honoring goodwill requests for long-term customers in good standing.

How long does a late payment stay on your credit report?

A late payment can remain on your credit report for up to seven years from the date of the delinquency under the Fair Credit Reporting Act. However, its impact on your score diminishes over time — a late payment from five years ago has far less impact than one from six months ago. A successful goodwill removal eliminates it entirely, regardless of how recent it is.

Can I send a goodwill letter to a collection agency?

Goodwill letters are most effective when sent to original creditors — the bank, credit card company, or lender that originally issued your account. Collection agencies purchased your debt for a fraction of its value and have less incentive to honor goodwill requests. For collection accounts, a pay-for-delete agreement or a debt validation letter is typically a more effective strategy.

How many times can I send a goodwill letter?

There is no legal limit. If your first letter is declined, wait 60 days and try again — to a different department or contact within the same organization. Sending to the executive resolution office or the office of the president often yields better results than standard customer service. Be respectful and patient with each attempt.

Will a goodwill letter hurt my credit?

No. Sending a goodwill letter does not affect your credit score in any way. It is simply a written request. The creditor may review your account but this is not a hard inquiry and will not appear on your credit report. The only change to your report would be a positive one — if they honor the request and remove the late payment.

What if the creditor says they cannot remove accurate information?

You may hear this response. It is technically true that creditors are required by the FCRA to report accurate information — but nothing in the law prevents them from choosing to remove a negative mark voluntarily. That is a business decision entirely within their discretion. If you receive this response, politely acknowledge it and ask again — specifically requesting that they exercise their discretion to remove the mark as a courtesy to a valued customer.

Get the Complete Goodwill Letter Bundle

The three templates above are a starting point. The complete Goodwill Letter Bundle at ParalegalGuides.com includes five professionally formatted versions — each designed for a specific creditor type and situation:

• Version 1 — General late payment (any creditor)

• Version 2 — Medical hardship late payment

• Version 3 — Billing error or missed notification

• Version 4 — Mortgage or auto loan late payment

• Version 5 — Long-term customer loyalty appeal

GOODWILL LETTER BUNDLE — 5 PROFESSIONAL TEMPLATES

$15 · Instant Download · Editable Word Document

All 5 versions in one download. Formatted, professional, and ready to personalize in under 10 minutes. Used by consumers across all 50 states to remove late payments from Equifax, Experian, and TransUnion.

Need more than a goodwill letter? If you are dealing with debt collectors, unvalidated accounts, or collection items on your credit report, explore our complete Debt Validation Letter Pack — 7 letters covering every stage of the debt collection defense process.

→ View the complete Debt Validation Letter Pack ($19) at ParalegalGuides.com/templates

Educational use only. This article and the templates provided by ParalegalGuides.com are for educational and informational purposes only. They do not constitute legal advice and do not create an attorney-client relationship. Laws vary by state. For advice specific to your situation, consult a licensed consumer rights attorney in your jurisdiction. © 2026 ParalegalGuides.com — Charles Storks, Paralegal.