Saving money is almost always framed as a discipline problem. If you can’t save, the unspoken assumption is that you’re irresponsible, impulsive, or just "bad with money."

You’ve probably told yourself this story before, especially after another month of good intentions that didn’t quite stick. Maybe you started strong, felt motivated, and then life happened. Groceries cost more than expected, something unexpected popped up, or you just needed a break. Slowly, saving slid to the bottom of the list again.

And each time it happens, the shame gets a little heavier. That story is very convenient, but it’s wrong.

It puts all the blame on you while ignoring the bigger picture. It assumes that if you just tried harder, stayed more disciplined, or wanted it badly enough, saving would magically happen. But most people don’t struggle with saving because they lack willpower. They struggle because they were never given a system that works with real life and I mean real bills, real stress, and real priorities.

No one teaches you how to save when money already feels tight. So instead, people internalize the failure and keep trying the same broken approach.

The Lie We’ve Been Told About Saving

From an early age, some of us were taught to save whatever is "left over" at the end of the month. The advice sounds simple enough: pay your bills, live your life, and if there’s anything remaining, that is what you save.

On paper, it feels logical and responsible. In reality, it sets you up to lose before you even begin. Because saving becomes conditional. It becomes something you do only if everything else goes perfectly. And we know life rarely works that way.

The problem is that there’s almost never anything left. Expenses expand to match your income, even when you’re trying to be careful. Costs rise, emergencies pop up, and those small "just this once" purchases quietly add up (trust me, I've been there). Saving turns into an afterthought instead of a priority.

Over time, this creates a frustrating cycle: you start strong, fall off, feel discouraged, and then promise yourself you’ll try again next month (you know you have). It's not because you failed, but because the strategy itself was flawed from the start.

Once you understand that saving isn’t a character flaw or a lack of discipline, something important shifts.

The shame starts to loosen its grip, and curiosity takes its place. If willpower isn’t the problem, then what is? And more importantly, what actually works for people who have real lives, real obligations, and real exhaustion?

The answer isn’t trying harder or cutting out every enjoyable thing. It’s changing the way saving is structured so it no longer relies on how you feel in the moment. Because feelings fluctuate, but systems don’t.

Motivation Isn’t the Missing Ingredient

Let's be real, motivation is unreliable by nature.

It comes and goes, often without warning. Some weeks you feel focused, disciplined, and determined to "get it together." Other weeks you’re tired, overwhelmed, juggling responsibilities, or simply trying to survive through the day. That doesn’t make you lazy, it makes you human.

The problem is expecting motivation to show up consistently enough to support long-term financial habits.

When your ability to save depends on how motivated you feel, saving will always feel inconsistent.

I've been guilty of this, you save during your "good" weeks and fall off during the hard ones. Then guilt creeps in, followed by self-criticism and another attempt to start over. This emotional rollercoaster keeps you stuck in the same loop, convincing you that you just need more discipline next time. But the truth is, motivation was never designed to carry something as important as your financial future.

What actually works is removing emotion from the process. When saving is automated, pre-decided, or visually structured, it no longer asks anything of your energy or mood. You don’t have to feel inspired or disciplined to follow through. The decision has already been made for you. And that’s when saving stops feeling heavy and starts feeling doable. And that my friend, is powerful.

Why Structure Changes Everything

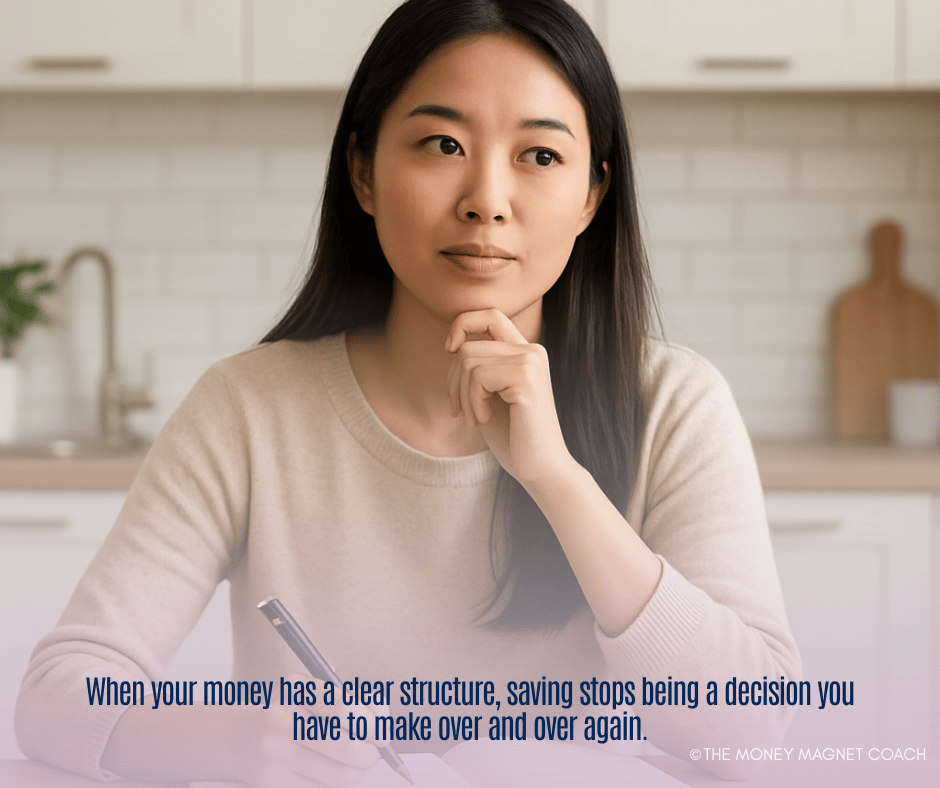

Structure is what turns good intentions into consistent action. When your money has a clear structure, saving stops being a decision you have to make over and over again. There’s no mental debate, no second-guessing, and no guilt attached to "failing" on a bad week.

Instead of constantly asking yourself, "Should I save this week?" or "Can I afford to put something aside?"

The answer is already built into your plan. You don’t rely on memory, motivation, or mood. With structure, the next step is always clear.

You’re no longer telling yourself, "I'll start next paycheck," because starting isn’t something you postpone, it’s something that’s already in motion. The plan accounts for real life, not a perfect version of it. It creates a rhythm that feels supportive instead of restrictive. And over time, that rhythm builds momentum without burnout.

This is what structure creates:

- Consistency without pressure, because you’re not forcing yourself to decide every time

- Progress without perfection, because missing a moment doesn’t derail the whole plan

- Calm instead of anxiety, because you know where your money is going

Most importantly, structure creates trust with yourself. Each follow-through, no matter how small, becomes proof that you can rely on you. And that trust is the foundation of real financial confidence.

Understanding the role structure plays in saving naturally leads to the next question: What does that actually look like in real life?

For some people, structure comes through automation or strict budgeting tools. For others, it comes through visual systems that make progress tangible and easy to follow. What matters most isn’t the format, it’s having a repeatable framework that removes decision fatigue and keeps saving moving forward even when life gets busy. When you can see your progress and know exactly what step comes next, saving becomes something you return to instead of something you avoid.

This is why simple, guided systems tend to work better than open-ended advice. They don’t ask you to "figure it out" on your own. They give you a plan, a rhythm, and a sense of momentum, without requiring perfection.

You’re Not Bad With Money; You’re Missing a System

If saving feels hard, it’s not a personal failure. It’s a signal that your money needs clarity and not criticism. So many people carry unnecessary guilt around their finances, assuming they’re the problem when the real issue is the lack of a supportive structure. Money is emotional, practical, and deeply tied to daily life, which means it needs systems that account for all of that, not shame or self-blame.

This is why I stopped trying to "be better" with money and shifted my focus to building repeatable habits instead. Once I had a system that worked with my real life, not an ideal version of it, saving stopped feeling heavy. It stopped feeling like something I had to force myself to do. Over time, it became automatic, predictable, and even empowering.

This the shift most people actually need. This is the shift I work to empower my clients to embrace.

Not more restriction. Not more guilt. Just a better way to organize their money in a way that feels doable and sustainable. When saving has structure, everything else feels lighter.

You stop second-guessing yourself. You stop starting over. And you begin building trust with your money decisions again.

If you’re ready to stop relying on motivation and finally put a system in place, the next step doesn’t have to be complicated. I created a self-guided savings challenge workbook to help you turn intention into action — one small, repeatable habit at a time. You don’t need to overhaul your life. You just need a place to start.

👉 You can explore the savings challenge workbook here.

Comments ()