5 Credit Score Killers (UK) — & How to Fix Them | Free Guide

Every month, thousands of UK residents are silently rejected for mortgages, credit cards and car finance. The reason? Almost always one of five fixable mistakes hiding on their credit file.

This free guide reveals exactly what those five mistakes are — and how to fix them, starting today.

WHAT YOU GET:

- ✓ 5-page PDF guide — instant download

- ✓ Actionable fixes for each mistake

- ✓ Written in plain English — no jargon, no paid service needed

Read it in 10 minutes. Apply the fixes this weekend.

WHO IS THIS FOR?

This is for you if:

- You've been rejected for credit and don't fully understand why

- You've never checked your credit file — or checked once and felt overwhelmed

- You're planning to apply for a mortgage, car finance or credit card in the next 6 months

- You want to fix your credit the right way, without paying for expensive services

WHAT'S INSIDE — THE 5 CREDIT KILLERS:

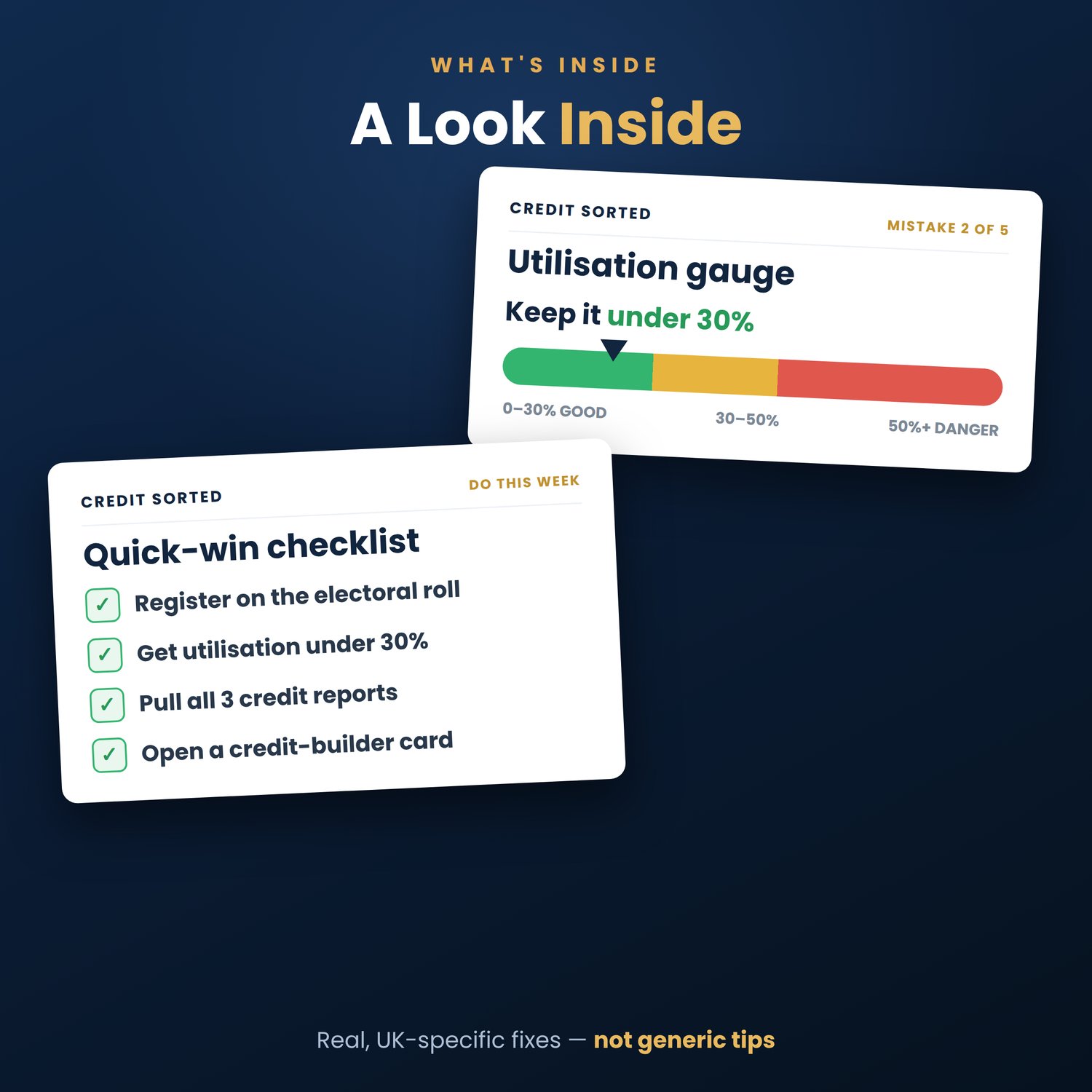

Mistake 1: You're Not on the Electoral Roll

The single highest-impact, zero-cost fix available. Lenders use the electoral roll to verify your identity and address. If you've moved in the last two years your registration has almost certainly lapsed — costing you points you don't know you're missing. The guide shows you the 5-minute fix.

Mistake 2: Your Credit Utilisation is Too High

Above 30% signals financial stress to lenders. Above 50% it actively damages your score — even with a perfect payment history. Inside, you'll get the exact way to fix your ratio, including a lender trick most people never think to try.

Mistake 3: Errors on Your File — That You've Never Checked

1 in 3 UK credit files contains at least one error. Experian, Equifax and TransUnion all hold different data — an error at one bureau won't show at the others. Under UK GDPR you have a legal right to dispute anything inaccurate, and the lender must respond within 28 days. The guide shows you how.

Mistake 4: No Visible Credit History

A thin file is treated almost as poorly as a bad one. If lenders can't see how you behave with credit, they assume the worst. Inside: exactly how to build a visible, positive track record — even if you've been burned before.

Mistake 5: Old Negative Markers You've Done Nothing About

Defaults, missed payments and CCJs stay on your file for six years from when they were registered — not when you paid them off. A debt cleared in 2022 can drag your score until 2028. The guide covers what you can legally do about it.

FREE TO DOWNLOAD. NO SPAM. UNSUBSCRIBE ANYTIME.

Instant download — no account required.

⚠️ Educational resource only. Not regulated financial advice under FSMA 2000. For free debt support, contact StepChange (stepchange.org) or Citizens Advice (citizensadvice.org.uk). For data rights queries, contact the ICO (ico.org.uk).