The 14 Day Money Leaks Killer

The 14-Day Money Leaks Killer

The 14-Day Money Leaks Killer

A mobile-native PDF workbook that finds where your money is leaking — across seven specific categories — and shuts the leaks off in fourteen days, with cancellation receipts and an automated transfer schedule as proof.

The promise

By the end of fourteen days, you will have at least $200/month redirected from leaks into savings or debt payoff — verified in writing through cancellation emails, bank screenshots, and a recurring auto-transfer.

Most buyers hit $300–$500/month once the non-obvious moves on Days 6, 8, and 9 are done. Receipts, not estimates.

If you make decent money and you're still broke at the end of the month

You're not lazy. You're not bad with money. The reason your account is empty by the 28th is that money is leaking through seven specific categories at the same time — and most of them are invisible until you look.

Subscriptions you forgot. Bank fees you didn't know you paid. The 22% APR on a card you've been "going to pay off" for two years. The $45/month you're overpaying on auto insurance because you haven't shopped quotes since 2021. The DoorDash receipts that look small one at a time and add up to $400/month. The Amazon orders you don't even remember.

This workbook isn't a budget. It isn't financial advice. It's a fourteen-day audit-and-cut protocol that finds every leak across all seven categories and shuts them off — most with one phone call or one click each.

You won't change your lifestyle. You'll change a small set of behaviors and recurring charges that are quietly costing you thousands a year.

What's inside

Fourteen days. Each day is one screen on your phone, five to fifteen minutes of work, one specific exercise you do in your notebook, and one micro-action — usually a cancellation, a phone call, or an account switch.

Days 1–3 — Diagnose

- Day 01 — The seven leak categories. Identify which categories leak in your life. Set up the leaks tracker.

- Day 02 — The Reality Check. WANT, WIN, BLOCK, MOVE, applied to dollars. RESTART NOW's signature exercise.

- Day 03 — The if-thens. Pre-decide responses to your three biggest spending triggers.

Days 4–6 — Excavate and cut the obvious

- Day 04 — Excavate 90 days of statements. The single most important exercise in the workbook. Mental accounting (Thaler, 1985) made literal.

- Day 05 — The subscription guillotine. Cancel 5–12 subscriptions. $30–$120/month redirected.

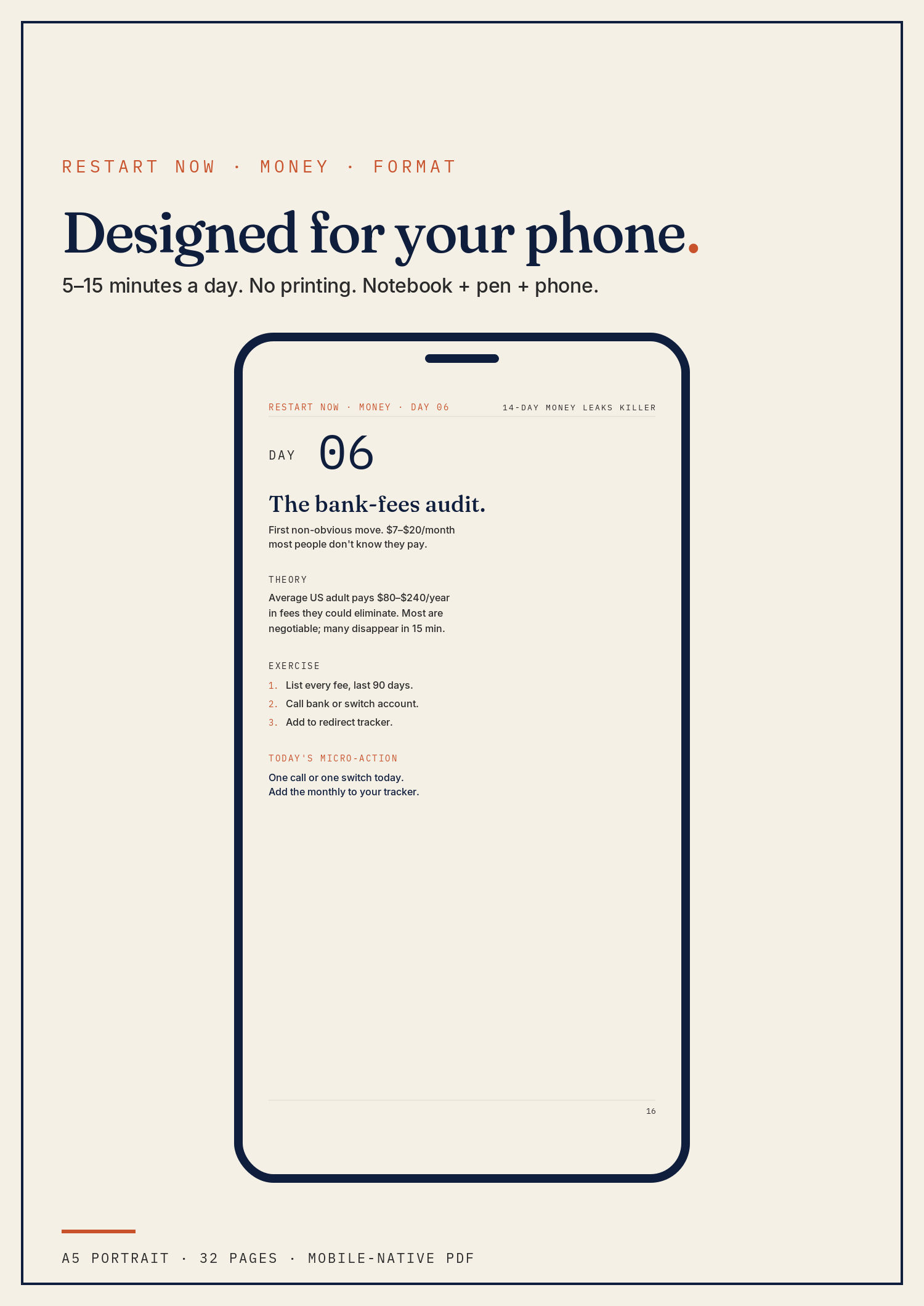

- Day 06 — The bank-fees audit. First non-obvious move. $80–$240/year that almost no one audits.

Day 7 — First review

- Calculate redirected total. Apply the right branch. Decide what to adjust.

Days 8–11 — The bigger non-obvious moves and the behavior fixes

- Day 08 — The interest extraction. Second non-obvious move. Outgoing (credit card APR via balance transfer) + incoming (high-yield savings vs 0.01% checking). $50–$150/month.

- Day 09 — The lazy tax. Third non-obvious move and the biggest single category for most adults. Auto/home insurance, phone, internet — overpaid by $1,200–$2,400/year.

- Day 10 — The food-delivery audit. The 40–60% premium most people don't see. Set a monthly cap.

- Day 11 — The 24-hour rule. Impulse purchases over $50 sit on a wishlist for a day. ~70% of items drop from intention.

Day 12 — Lock it in

- Set the auto-transfer that captures the redirected amount and moves it to savings or debt every payday +1.

Days 13–14

- Day 13 — Review and expand. Tally. Branch. Identify next leaks.

- Day 14 — Entrench. Identity statement, three high-risk responses, 30-day calendar check-in.

Plus a contents page, a leaks tracker template, a what-to-expect orientation, an FAQ, a troubleshooting page, and a citations section.

Built on real research

This workbook is grounded in three behavioral-economics findings that are robust across hundreds of studies.

The research it's built on:

- Default bias — Thaler & Sunstein, Nudge (2008). Most people stay with whatever is currently set up. The fix: deliberately break the default once.

- Mental accounting — Thaler (1985). $14.99/month feels small alone; $180/year doesn't. The fix: force the annual view.

- Implementation intentions — Gollwitzer & Sheeran (2006). 94-study meta-analysis. If-then plans roughly double goal-achievement rates.

- Money scripts — Klontz et al. (2008). Behavioral framing of avoidance and spending patterns.

- Self-perception theory — Bem (1972). Identity-based change outlasts outcome-based change.

If you want to go deeper after Day 14, the resources page lists Ramit Sethi's I Will Teach You to Be Rich (the standard automation playbook) and how to find non-profit financial counseling through the National Foundation for Credit Counseling.

Who this is for

Adults 28–50, household income $50K–$200K, employed, paycheck-to-paycheck despite stable income. Actively looking for ways to save without giving up your life. Has tried Mint, YNAB, or Monarch and abandoned them. Wants a structured, evidence-based protocol they can run themselves in two weeks.

Who this is not for

This workbook is not:

- a budget. No tracking after Day 14, no envelopes, no spreadsheet.

- financial advice. We don't tell you what to invest in.

- a debt-payoff plan (that's The 14-Day Debt Plan).

- a workbook for households earning under the federal poverty line — when the issue is income, not leaks, the protocol doesn't help.

If your income is below your essential expenses (rent, utilities, food, transport), see a non-profit financial counselor at the National Foundation for Credit Counseling (nfcc.org) instead. Free, the right tool for that situation.

The format

A 32-page, A5 portrait, mobile-native PDF. Designed to read on your phone at fit-to-width — no pinch-to-zoom, no printer required. Each day's screen is dense with teaching and prompts; you write your answers in a separate notebook, not in the PDF.

You'll need three things:

- A notebook (any notebook — bound, spiral, the back of a calendar).

- A pen.

- Your phone — for reading the PDF, the cancellations themselves (most are killed in three minutes from the bank app), and the recurring alarms the protocol depends on.

Don't print the PDF. It's designed for using it on mobile phones.

FAQ

What if my income is the problem, not leaks? This workbook can't solve a structural income gap. If your essential expenses exceed your income, see a financial counselor at nfcc.org.

Do I need a budgeting app? No. The auto-transfer (Day 12) does the work of a budget. After Day 14 you only need a monthly 30-minute statement review.

What about Mint or YNAB? Both are fine, neither is required. Mint shut down in 2024; YNAB works for buyers who like tracking. The protocol does not depend on either.

What if I can't get a 0% balance-transfer card? Your credit may need work first. Skip Day 8's outgoing-interest move; do the incoming-interest move (high-yield savings) instead. Revisit in 6 months.

What if my partner won't cooperate? Run the workbook on accounts you control. Auto-transfer from your individual account. Bring the partner in once you have 30 days of redirected dollars to show.

Refunds. If the PDF doesn't open, doesn't render correctly on your phone, or you decide it's not what you expected, email within 30 days and you'll get a refund. After 30 days you've either followed the protocol or you haven't — the workbook is the workbook.

What you'll have at Day 14

- 5–12 subscriptions cancelled with confirmation emails.

- Bank fees zero'd or near-zero.

- Credit-card interest extracted via balance transfer; cash moved to high-yield savings.

- 1–3 lazy taxes cut — insurance, phone, internet.

- A monthly food-delivery cap and friction added to apps.

- The 24-hour rule active; "buy now, pay later" apps deleted.

- An auto-transfer to savings/debt running on payday +1.

- A signed identity statement and a 30-day calendar entry already scheduled.

Most buyers hit $300–$500/month redirected — $3,600 to $6,000 a year, recovered, automatically, every year, going forward.

The protocol is not the workbook. The protocol is the auto-transfer + the 24-hour rule + the monthly statement review, running for the next thirty days. The workbook just made it explicit.

The 14-Day Money Leaks Killer · 32-page mobile-native PDF · $27