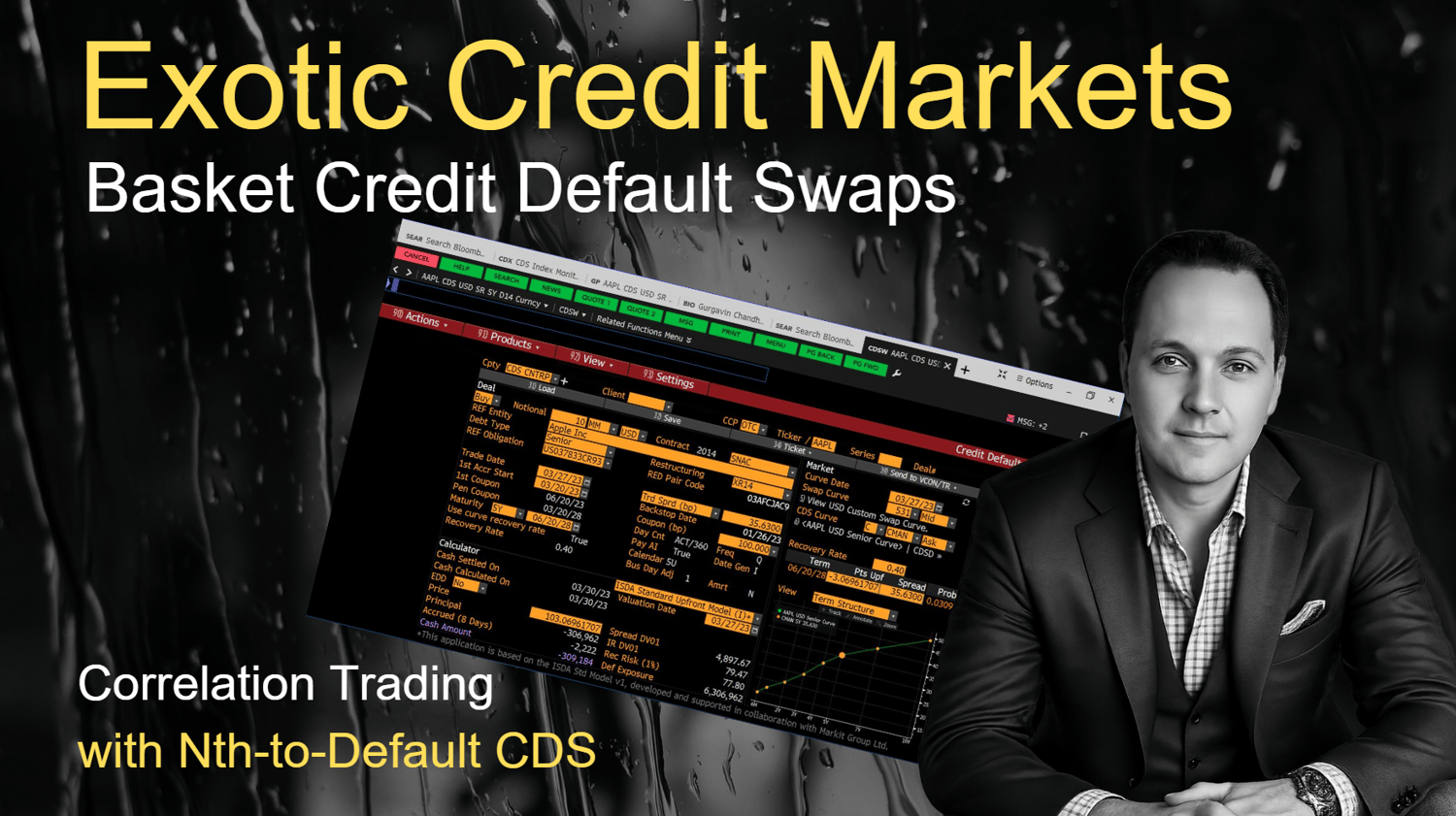

Professional Training - Exotic Credit Markets & Basket Credit Default Swaps

Excel Workbook & Guide

Contents

- Nth-to-Default CDS - Excel Workbook

This workbook contains the following Quant models and products:-

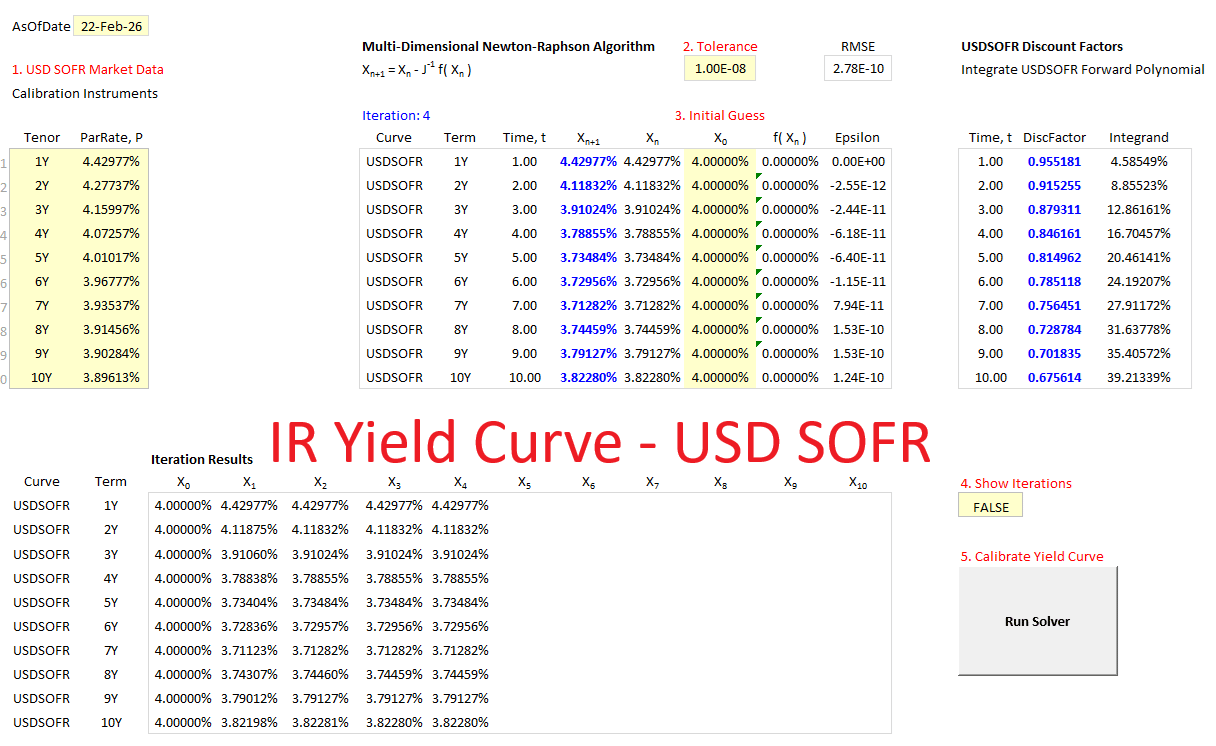

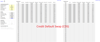

- IR Yield Curve Model, USD SOFR

- Interest Rate Swap Pricer

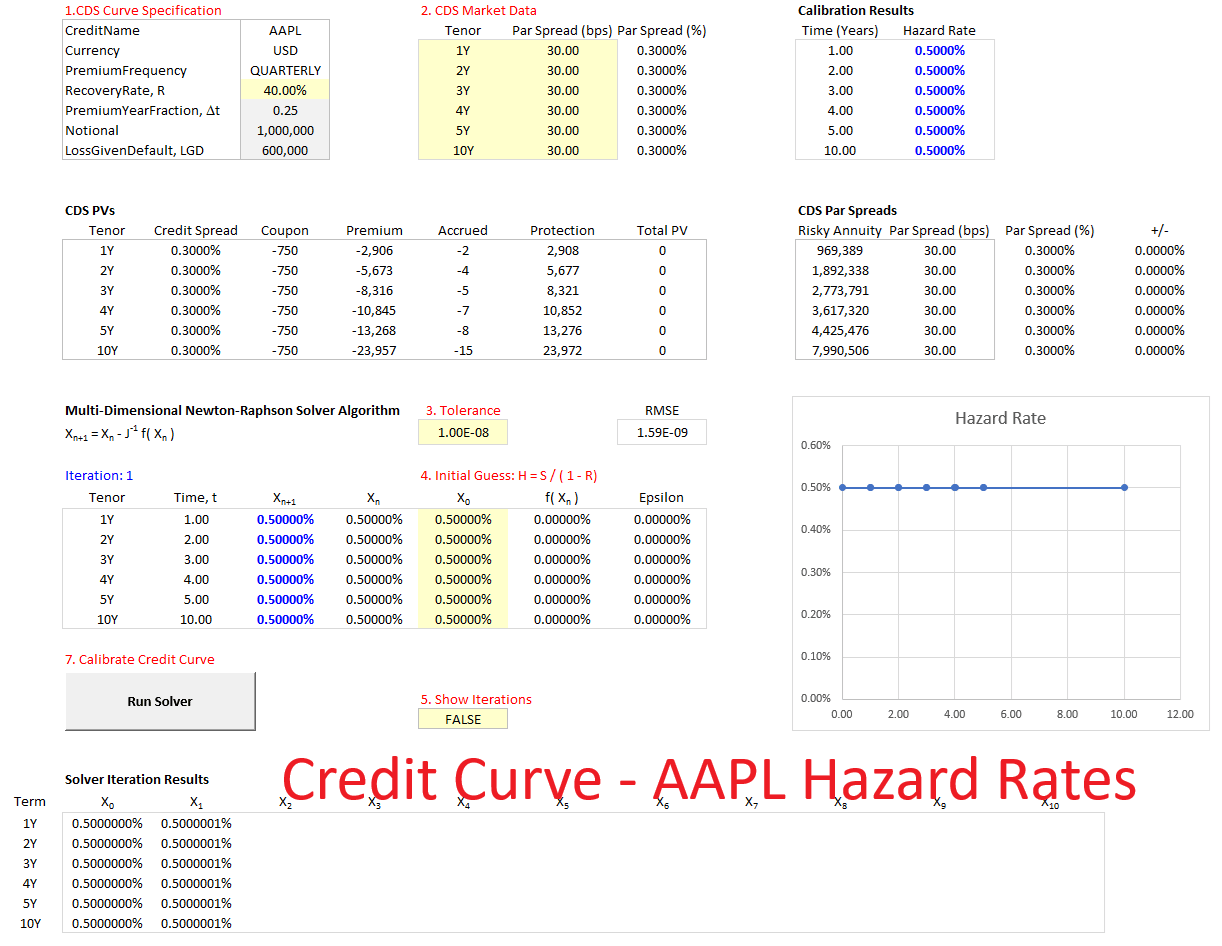

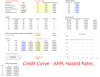

- Credit Curve Models

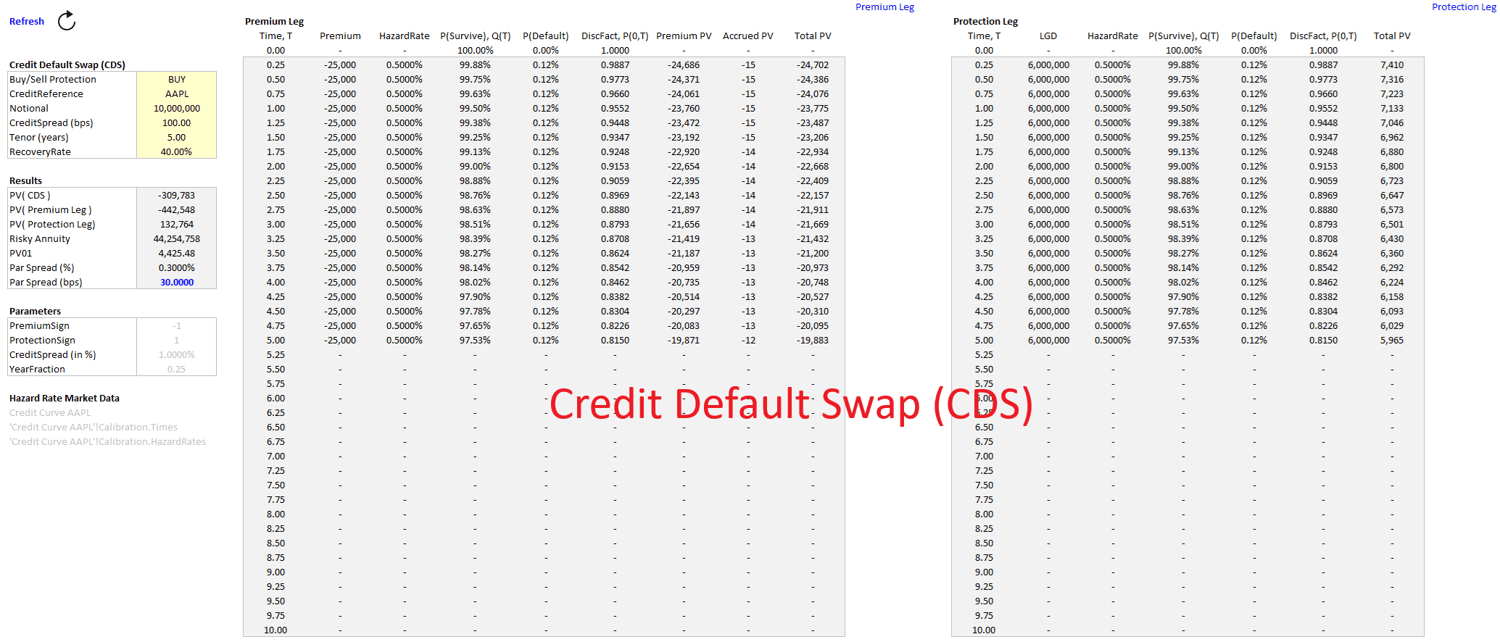

- Credit Default Swap Pricer

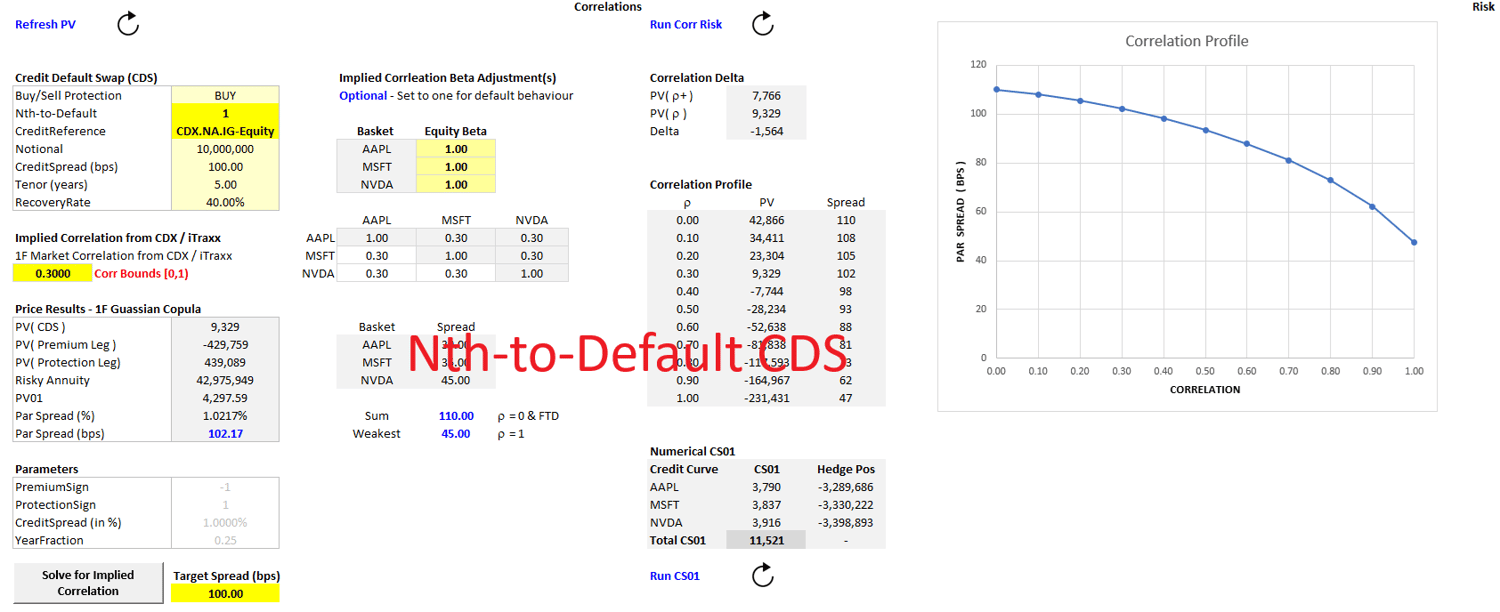

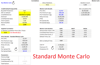

- Nth-to-Default CDS Pricer - Analytical 1F Gaussian Copula

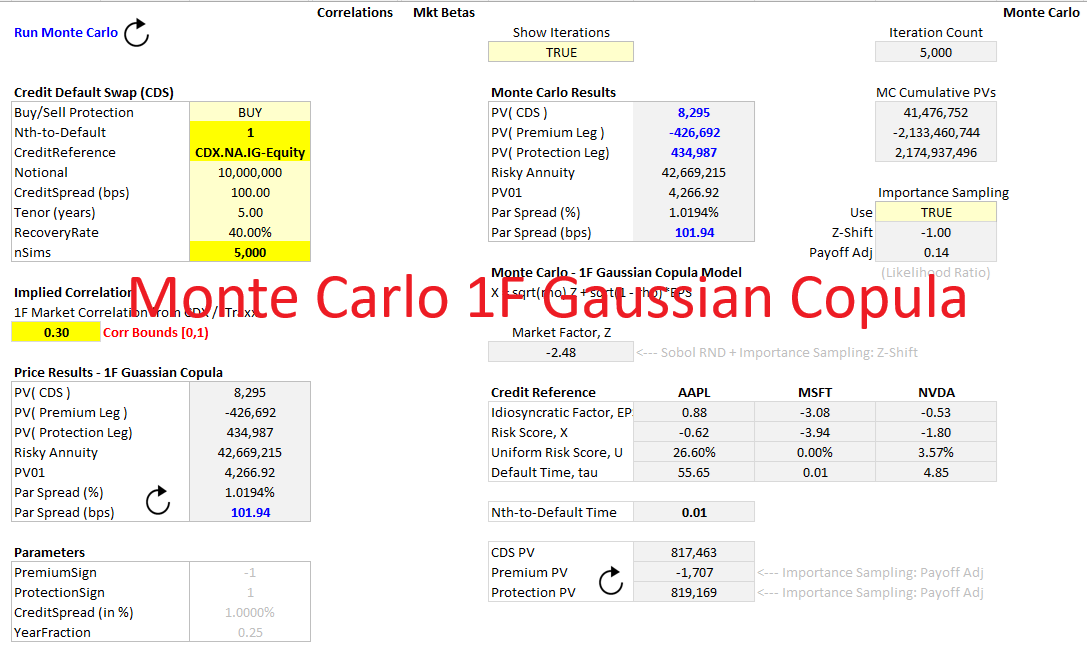

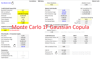

- Nth-to-Default CDS Pricer - Monte Carlo 1F Gaussian Copula

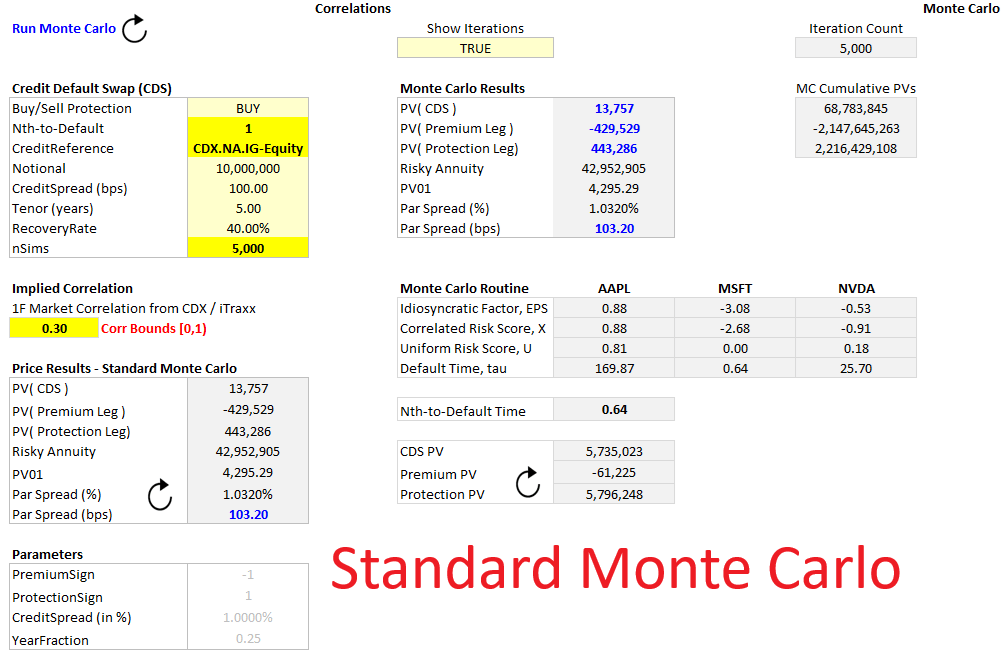

- Nth-to-Default CDS Pricer - Monte Carlo with Cholesky Decomposition

Excel Pricing Workbook Overview

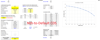

This Excel workbook is a practical, front-to-back implementation of how professionals price and trade correlation-driven credit products, centred on the Nth-to-Default (NTD) CDS. Using a live credit basket comprising of Apple (AAPL), Microsoft (MSFT) and Nvida (NVDA), the model walks through the complete build: constructing a USD SOFR interest rate curve for discounting, demonstrating its use in IRS valuation, and then calibrating single-name credit curves consistent with that yield curve. From these curves, hazard rates (instantaneous default intensities) are derived to compute survival and default probabilities, forming the foundation for rigorous CDS pricing.

The workbook progresses from vanilla CDS valuation to basket CDS pricing, including 1st-, 2nd- and 3rd-to-Default structures. It implements the analytical 1-Factor Gaussian Copula framework introduced by David Li (2000), solved via numerical integration, alongside two Monte Carlo approaches: a 1-factor copula simulation and a full Cholesky-based correlated normal framework. By explicitly modelling market-implied correlation, the model shows how NTD spreads transition between single-name risk (high correlation) and diversification-driven behaviour (low correlation), providing direct insight into dispersion and correlation trading strategies.

Designed for practitioners, students, and quants, this workbook is both an educational deep-dive and a trading laboratory — a rare, transparent implementation of tools typically confined to bank credit desks.

Keywords:

Nth-to-Default CDS Excel model, First-to-Default pricing spreadsheet, basket CDS valuation, credit correlation trading, Gaussian Copula implementation, 1 Factor Copula David Li, Monte Carlo CDS simulation, Cholesky correlation model, credit derivatives analytics, SOFR yield curve construction, hazard rate calibration, credit curve bootstrapping, survival probability modelling, exotic structured credit products, dispersion trading strategy, implied correlation analysis, quantitative finance toolkit, credit risk modelling, fixed income derivatives valuation, multi-name CDS pricing, financial engineering template, professional correlation trading model