AT1 Contingent Convertible Bonds - Exotic Monte Carlo Pricing

On Sale

£35.00

£35.00

Python Code, Jupyter Notebook & Guide

Contents

- CoCo Bonds - Python Source Code

- CoCo Bonds - Jupyter Notebook

Jupyter Notebook & Guide

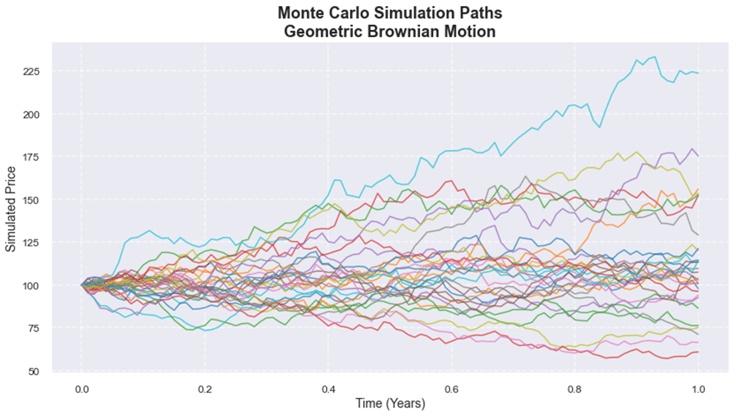

This notebook provides a practical, hands-on guide to AT1 Contingent Convertible (CoCo) Bonds. It combines financial modelling theory with Python code to illustrate the pricing of these exotic hybrid instruments using advanced Monte Carlo simulation.

C++ Version

For a complimentary C++ version that can be run using a free online compiler, see https://onlinegdb.com/m62t3nbn6.

Notebook and Guide Objectives

The notebook and accompanying documentation are designed to help you:

- Understand the features, mechanics, and risks of AT1 CoCo Bonds, including conversion triggers and issuer call options.

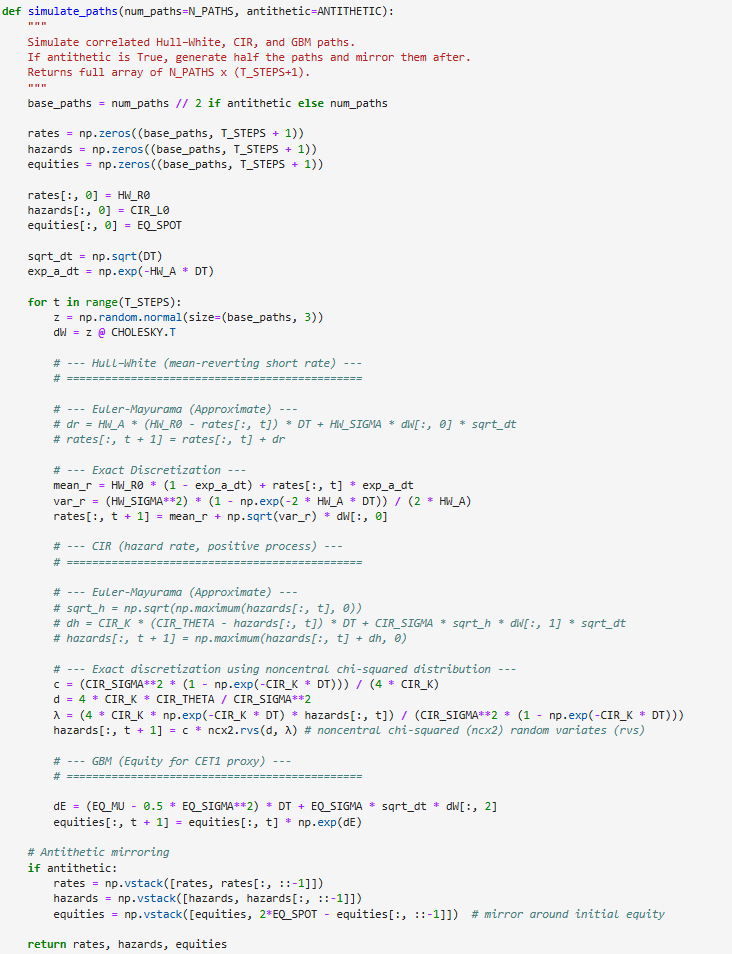

- Learn how to model multiple risk factors using a 3-factor framework:

- Extended Hull–White for interest rates

- CIR model for credit/hazard rates

- Geometric Brownian Motion (GBM) for equity / CET1 ratio proxy

- Implement exact simulation Monte Carlo, correlating model drivers via Cholesky decomposition.

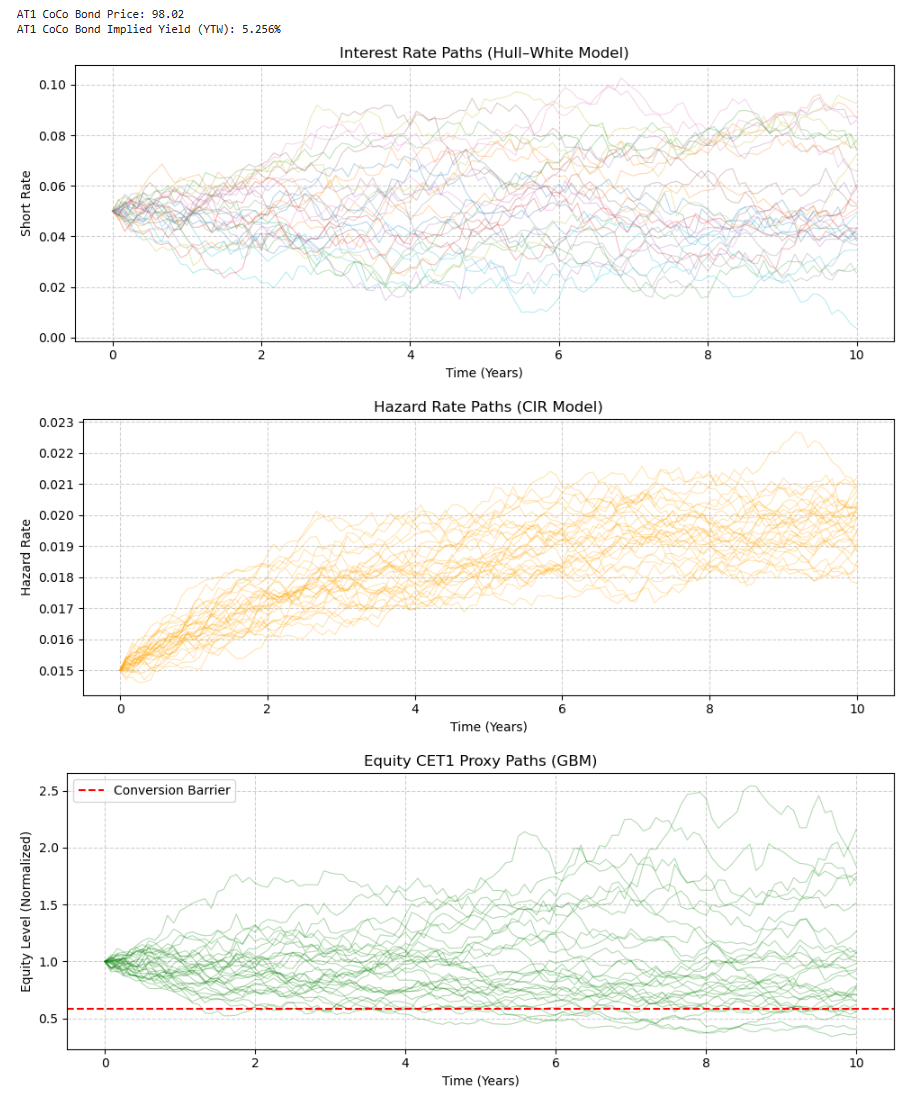

- Compute the Coco Bond PV, incorporating embedded issuer call and regulatory contingent options.

- Explore diagnostics and visualization: price convergence, path plots, and comparison against a vanilla fixed bond to understand exotic features.

Keywords:

- AT1 CoCo Bonds, Contingent Convertible Bonds, Monte Carlo Simulation, Hull–White, CIR Model, Equity Proxy, Exact Simulation, Cholesky Decomposition, Pricing, Yield Analysis, Embedded Options, Path-Dependent Instruments, Financial Risk.